No. 53, May 2013

| |

|

|

No. 53, May 2013 |

|

|

No. 53 Why Do Credit Rating Agencies Press India to Reduce Government Spending? The 'Fiscal Deficit' Bogeyman and His Uses Large Corporate Firms on Investment Strike, Playing with Cash Will Cutting the Fiscal Deficit Bring Down Inflation? What Is Missing in the Present Discussion

|

The Two Aims of the Budget The Budget has in the main two explicit aims, as stated in Chidambarams Budget speech. The first is to attract foreign capital at all costs:

The second is to revive growth by getting private investors to invest:

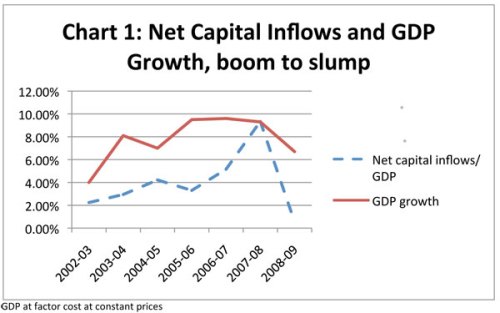

The key to understanding the Budget as well as the entire range of economic policies being pursued by the Government lies in these two statements. The language of these statements subtly makes clear the hierarchy of priorities. Foreign investment is an imperative, i.e., it must be obeyed; whereas growth is the highest goal. The golden era of 2003-08 In this period, foreign capital flooded into India, and as it did it propelled share markets and real estate prices upward, making some people much richer. Banks, flush with funds, pressed loans on retail customers for flats and cars. Drunk with optimism, the Indian private corporate sector borrowed and invested in new projects as if this expansion would last forever. The Index of Industrial Production and the Gross Domestic Product soared. The common people did not get much benefit from all this development rather, they had to pay its costs in manifold ways; but for Indias ruling class it was a golden era.

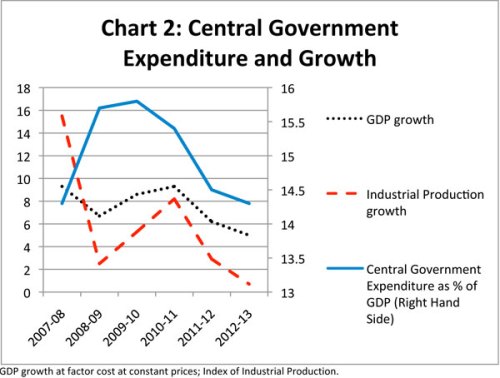

Slump All that changed with the collapse of the US investment bank Lehman Brothers in 2008. The music of liquidity stopped, and the financial sector stood at the brink of disaster. At this point governments in all the leading economies, in particular the US, Europe and Japan, declared it was absolutely critical to funnel huge public funds to the financial sector (without, of course, nationalising it). This required an expansion of spending by governments and bail-outs by the central banks. Various estimates have been made of the total sum doled out from the worlds treasuries and central banks to the financial firms; they all run into many trillions of dollars. Once the financial sector was rolling in public money again, however, it called a halt to government spending, warning ominously of the danger of inflation if governments paid for teachers salaries, healthcare, and other public employment. Throughout the world, austerity was the new slogan, even though this merely reduced already inadequate demand and plunged various countries, particularly European ones, deeper into unemployment and mass misery. In India, the global crisis quickly punctured all the fancy theories of decoupling i.e., the claim that the growth of Third World economies like Indias was being powered by a separate dynamic from that of the wealthy countries. It deflated the notion that the tiger of Indian growth had been unleashed by liberalisation and globalisation, and that the new-age Indian entrepreneur now strode the world like a colossus. It turned out, on closer examination, that India was hardly unique; the whole world had grown in the post-2001 period with the flood of liquidity from the developed countries. And when the crisis struck in the US, foreign capital promptly retreated from India for safer havens. Indias share market indexes plunged to well below half their peak levels. Industrial growth dropped from 15.5 per cent in 2007-08 to 2.5 per cent in 2008-09. The GDP fell a little less steeply, from 9.3 per cent to 6.7 per cent. Revival through Government stimulus As we noted above, in the immediate aftermath of the crisis, the financial sector worldwide temporarily withheld its objections to an expansion of government spending (since it was the main beneficiary). In this permissive climate, the international financial oligarchy allowed the Indian government to increase spending (even though the financial sector in India did not require a bail-out). The Finance Minister said he was pressing the pause button on the Fiscal Responsibility and Budget Management (FRBM) Act (which compels a steep annual reduction in Government borrowing/GDP). The expenditure of the Central government rose by about two percentage points of GDP in the first year of the crisis, and stayed at about that level up to 2010-11. GDP growth recovered smartly to 8.6 per cent and 9.3 per cent in 2009-10 and 2010-11. Thus, despite the dramatic drop in foreign capital inflows, the fiscal stimulus managed to revive growth. The Government immediately attributed this revival to the inherent strength of the economy. The Economic Survey 2010-11found that The Indian economy has emerged with remarkable rapidity from the slowdown caused by the global financial crisis of 2007-09…. the turnaround has been fast and strong…. the Indian economy is coming through with resilience and strength…. etc, etc. However, the Economic Survey 2012-13 recognises that the Indian economys recovery in that period was essentially a response to the stimulus, and that the boost to demand from this stimulus was substantial. Withdrawal of the fiscal stimulus; slump again Nevertheless, around the middle of 2010, international finance sent out the signal that Governments around the world must start withdrawing the fiscal stimulus they had provided their economies in the previous two years. The Indian rulers not only complied, but now parroted international finances arguments that expenditure-slashing (termed fiscal consolidation) was good medicine, and would actually boost growth. The Economic Survey 2010-11 thus looked forward to the reduction of Government spending, which it sunnily predicted would actually boost savings, investment and GDP growth: fiscal policy is on the consolidation path… and, going forward, this is likely to yield growth dividends in the medium to long term setting in motion a virtuous cycle…. The latest data on savings and investments, which pertain to 2009-10, show that these rates have turned around…. Since savings and investments now show a positive momentum and the Government is implementing a gradual exit from the stimulus package, the savings and investment rates are likely to rise further. Hence it is expected that the economys growth will breach the 9 per cent mark in 2011-12.

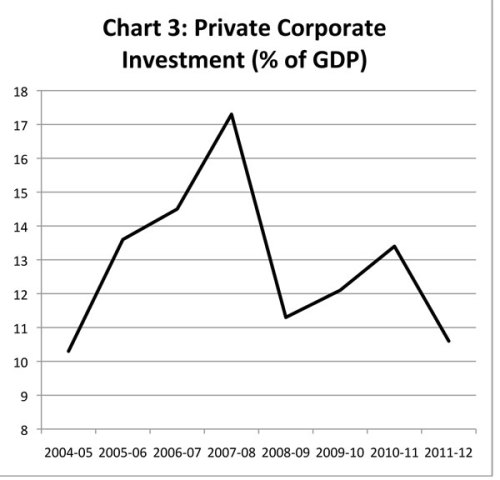

In line with this, Central expenditure was brought down to 14.5 per cent of GDP in 2011-12 and 14.3 in 2012-13. However, contrary to the predictions of the Economic Survey, the investment and savings rates promptly fell in 2011-12, and are certain to have fallen further in 2012-13 (for which we do not as yet have data). GDP growth, far from breaching the 9 per cent mark, fell even more sharply than it had in 2008-09. It managed a mere 6.2 per cent in 2011-12, and fell further to 5 per cent in 2012-13. Private corporate sector investment stalls During the 2003-08 boom, the private corporate sectors outlook had been buoyant; with easy access to funds, it expanded its investment from 10.3 per cent of GDP in 2004-05 to a giddy 17.3 per cent in 2007-08. Equally dramatically, it turned pessimistic in 2008-09, reducing investment to 11.3 per cent of GDP (in current rupee terms, it fell by Rs 2,25,000 crore). More significantly, even after the Government stimulus package revived GDP growth to the earlier peak of 9.3 per cent, corporate sector investment picked up only moderately; it did not return to its earlier peak. And with the second downturn in GDP in 2011-12, corporate sector investment plunged once more, to even an even lower percentage of GDP than in 2008-09. In current rupee terms, it fell Rs 90,000 crore between 2010-11 and 2011-12. The latest available data suggest that corporate investment has fallen even further in 2012-13: in the first nine months of the financial year, domestic capital goods (i.e., investment goods) production fell by 10.1 per cent over the corresponding period of the previous year, and in the first eight months, capital goods imports fell by 6.5 per cent.

Evidently, then, the global crisis that broke in 2008 and refuses to go away has shaken the private corporate sector. It is not confident that the earlier levels of growth and profit can be achieved. And so the corporate sector is refusing to invest its cash in physical investment such as plant and machinery. (See earlier article: Large corporate firms on investment strike, playing with cash.) The reason large firms are refusing to invest is that they are not sure their investments will be sufficiently profitable. The principal reason for this is that they anticipate that demand will be inadequate; in some sectors, it is so poor that they are retrenching production. (A stark example of this is the recent decision by some automobile firms to stop production temporarily.) And as the corporate sector postpones investment for lack of demand, demand gets depressed further, leading them to postpone investment yet further. Contradiction between assuaging foreign investors and boosting growth In these circumstances, an increase in Government spending can revive demand, sending industrialists the signal that once again there are more profits to be made in production than in playing with cash.This would prod them to return to investing in expanding productive capacity, and thus revive growth. Why then does the Government not increase its spending, and indeed why does it do the contrary? Foreign investors, particularly foreign financial investors, are pressing for a reduction in Government spending. The reason is not that they fear that the Governments fiscal deficits are unsustainable. If that were the case, they could as well call for increased taxation of corporations and the rich. Rather, they want Government spending reduced to create more opportunities for private profit-making, in which they will be sure to garner a large share. Low growth ahead In fact, international finance does not stop at insisting on a cut in Government spending. It even applies pressure to keep Indias interest rates high, in the name of checking inflation. The large difference between interest rates in India and in the developed countries strengthens the hands of foreign finance to make all sorts of gains in India (for example, it is able to borrow cheaply in the west and park large sums in relatively safe bonds here, earning a handsome margin). Large industry in India, on the other hand, is opposed to high interest rates, because they eat up part of its profits, and depress demand for its products (e.g., sales of automobiles, earlier driven by credit, have plummeted over the last year). Nevertheless, the Reserve Bank has not been listening to the pleas of domestic large industry. Three years ago it lent to the banks at 5.25 per cent; today (even after three recent reductions) it lends to them at the much higher rate of 7.50 per cent. This in turn keeps the rate at which banks lend to borrowers very high. As a result, those who are thinking of buying cars and flats tend to postpone their purchases; and this affects auto firms, real estate firms, and all those who produce materials for cars and buildings, and the goods that fill them up. Unlike financial capital, which can even feed off carrion, industrial capital generally needs some output growth in order to be able to make profits and accumulate capital (accumulation being the aim and reason for existence for all categories of capital). These contrary pulls are reflected in the contrary positions of Indian officials. The Finance Ministry, which tends to lend an ear to industrialists, has been pressing the RBI to lower interest rates. The RBI, which sees its role as the protector of foreign financial capital, has largely resisted such pressure. It has been demanding that, before it cuts interest rates, the Finance Ministry first suppress demand by cutting Government spending. Now that the Finance Minister, in line with the RBIs opinions, has slashed spending brutally in 2012-13 and promises to do more of the same in 2013-14, the RBI has responded by slightly reducing interest rates. However, the spending cuts carried out by the Finance Minister will tend to reduce overall demand, and thereby reduce the very growth that was meant to be generated through interest rate reductions. In other words, we are in for a spell of low growth. Thus, even though the Planning Commission in October 2011 set a target of 9 per cent average annual GDP growth for the 12th Plan (2012-17), and more recently finalised the target at 8 per cent, no one takes either figure seriously; the Prime Minister himself told Parliament on March 8 that he hopes that in two to three years, the economy will bounce back to high growth of 7 to 8 per cent. (emphasis added) Handling the contradiction between demand-suppression policies and need for growth How is this contradiction between the demand-suppression insisted on by international finance on the one hand, and domestic corporate capitals need for growth on the other to be handled? For all their disagreements, the RBI and the Finance Ministry are basically agreed on the approach: Instead of trying to boost overall growth, the State must attempt to boost private corporate sector growth (which is anyway its main aim in promoting overall growth) through specific measures targeted at it. It must try to trigger corporate investment by providing it tax subsidies, opening up hitherto restricted sectors (such as retail), accelerating acquisitions of land, and ramming through environmental clearances even in the face of resistance. It must take steps or formulate policies to make the creation of infrastructure (such as roads, power, oil/gas production, industrial zones, and sites for new cities) more profitable among other things, by raising prices of their products. This two-pronged effort at meeting the demands of fickle foreign speculative capital and yet reviving corporate sector growth is reflected in the latest Budget. I. A Budget addressed to FIIs In January 2013 , Chidambaram traveled to Singapore, Hong Kong, Frankfurt and London to meet foreign investors at gatherings arranged by FIIs Bank of America Merrill Lynch, Citigroup, BNP Paribas, and Deutsche Bank. Journalists were kept out, and the Indian press had to make do with press releases handed out by the hosts. In these intimate gatherings Chidambaram presented the revised figure for the 2012-13 fiscal deficit and the 2013-14 Budget figure for the fiscal deficit. Since then, Chidambaram has taken his road show to London, Frankfurt, Canada and Dubai, with Tokyo scheduled as the next stop. Clearly, the principal intended audience for the Budget was not domestic, but foreign. The principal (though far from the only) way in which the Budget aims to please foreign capital is by suppressing Government expenditure. (See separate note: "FIIs: Difficult to Please".) As a result, the food subsidy has barely been raised, despite the planned National Food Security Act; the fertiliser subsidy has been reduced; the petroleum subsidy has been cut (which will result in a general price rise); the entire range of developmental and welfare expenditure has been cut in real terms (i.e., after taking into account inflation) and in some cases in absolute terms; the Government is committed to carrying out an unprecedentedly large sale of public sector shares; and so on. Before the Budget, the Government set the public sector oil marketing firms on a course of hiking diesel prices every month until they reached market levels (over an estimated 18 months). It also increased rail fares. As was expected, these direct attacks on the real incomes of the working people won the immediate appreciation of foreign capital as well as the domestic corporate sector. II. Persuading the corporate sector to invest Chidambaram declares in his Budget speech: The growth rate of an economy is correlated with the investment rate.The key to restart the growth engine is to attract more investment, both from domestic investors and foreign investors. In other words, the revival of the economy lies entirely in the hands of the corporate sector, and all the Government can do is to keep it happy so that it agrees to invest. (i) The Budget aims to persuade the private corporate sector to invest in the building of physical assets plant, machinery, roads, railways, oil/gas wells and pipelines, and so on. The private corporate sector is to get subsidies on investment: On investment by manufacturing firms on plant and machinery of over Rs 100 crore, the Budget gives a 15 per cent investment allowance in addition to the current rates of depreciation. (One newspaper calculates the benefits to industry from the investment allowance alone at Rs 25,000 crore over the next two years, a sum equivalent to 7.3 per cent of the profits of the top 500 firms in the Bombay Stock Exchange in 2011-12.[4]) Power projects are given another year to come under the 10-year tax holiday scheme. There are also provisions for tax-free bonds for infrastructure. (ii) Some additional Government orders for infrastructural firms can be expected with the gargantuan industrial corridor projects. The Budget mentions in particular the Delhi-Mumbai Industrial Corridor Project (DMIC). This $90 billion behemoth will cover a band of 150 kms over six states on either side of the 1,483-km Dedicated Freight Corridor between Delhi and Mumbai. It involves the creation of seven new cities, nine industrial regions of 200-250 sq km each, 15 industrial areas of 100 sq km each, three ports, six airports, a six-lane intersection-free expressway and a 4,000 MW power plant. The funds are to come from Government expenditure, Japanese official loans, and private (including Japanese) investment. All this, of course, will require the acquisition of vast lands and grabbing of water resources along the corridor. (iii) A crucial incentive to the private sector to invest in infrastructure is the promise of higher tariffs. The most prominent instance of stalled corporate investment is Reliances failure to develop the KG-D6 gas field in the Krishna-Godavari basin until the Government revises upward the price it gets for the gas. Despite the Rangarajan committee having recommended more than doubling the price that producers should get, Reliance is still not entirely satisfied. The Budget speech mentions that The natural gas pricing policy will be reviewed and uncertainties regarding pricing will be removed. Further, as mentioned above, the Government embarked in January 2013 on a course of hiking diesel prices every month for 18 months. The Budget speech announced that the cost of expensive imported coal will now be pooled with domestic coal. The higher costs of imported coal will distributed over the costs of all power plants, thus bailing out new private sector power projects; if implemented, this will result in a rise in all power tariffs. Private sector power firms are also expected to benefit from the restructuring of bank debt of state electricity boards. These debts are being restructured on the condition that they raise their power tariffs. The Budget also announces that the private sector is to be involved in coal mining, through public-private partnerships with Coal India; inevitably, coal prices will be raised in order to incentivise private investors. All these measures are going to place further burdens on the mass of working people in the cause of boosting corporate profits. The main source of inflation in the coming period is likely to be from price hikes of fuel and infrastructure. Why is the Government today placing particular stress on boosting infrastructural investment? The reason is that (i) the Governments spending cuts make it impossible to boost consumer demand in general; and (ii) the RBIs persistence with high interest rates makes it impossible to fuel middle-class credit-driven spending on flats, cars, and other consumer durables. Infrastructure, on the other hand, can be made profitable for the corporate sector even when overall demand is poor, if infrastructural firms are able to extract high prices on the basis of its monopoly status, State subsidies, and overall capture of State policy-making. (iv) As part of this overall thrust, the Government is doing all it can to accelerate clearances for large projects, driving a truck through the environment and tribal ministries. Particularly striking is the manner in which the Prime Ministers Office has made a mockery of one of the UPA Governments flagship legislations, the Forest Rights Act. (See Annexe: Growth through Plunder: Recent Measures regarding the Forests.) Indias much-hyped growth story since 2003 has had a large component of corporate plunder of natural resources, forcible acquisition of peasant land, and destruction of the environment.[5] Scholars have searched for words to describe this phenomenon: for example, accumulation by dispossession,[6] accumulation by encroachment,[7]predatory growth.[8] In the present phase of low growth, there is even less scope for growth through normal means. Hence the even greater importance of growth through encroachment, dispossession, predation. This implies sharper conflicts between those accumulating and those being dispossessed. The recent terror and mayhem being inflicted on the villagers resisting eviction by POSCO in Odisha is a stark example of this. Addressing probationers of the Indian Police Service in December 2010, the Prime Minister made clear the connection between their duties and the broader economic mission of the countrys ruling classes: You belong, he said, to a very privileged Service, along with the IAS, and the Forest Service you are three All India Services…. Naxalism today afflicts the Central India parts where the bulk of Indias mineral wealth lies and if we dont control Naxalism we have to say goodbye to our countrys ambitions to sustain growth rate of 10-11 per cent per annum…[9] According to news reports, a surge of security forces will soon bring the total central forces in these areas of mineral wealth to nearly 1,00,000, a figure comparable to the number of western forces fighting to stabilise Afghanistan.[10] This vast, multi-pronged exercise of shifting the burden of the current crisis on to the backs of the people, by reducing their social claims (through spending cuts), reducing their real incomes (through inflation), and plundering their resources and livelihoods, may yet not succeed in reviving the corporate economy. Given the absence of stimulus from Government expenditure, and the increasing paucity of purchasing power of the working people, that revival may yet await a fresh bubble from abroad. Annexe: Growth through Plunder: Recent Measures regarding the Forests Among the steps taken by the Government during the last few months are as follows: (i) On December 13, 2012, the Government set up a Cabinet Committee on Investment (CCI) headed by the Prime Minister for fast-tracking decisions on projects of over Rs 1,000 crore. This fast-tracking essentially involves removing the obstacles placed by the existing laws, particularly regarding environment, displacement, and the rights of forest dwellers.[11] Neither the Minister of Environment and Forests nor the Minister for Tribal Affairs is a member of the CCI; while the former is an invitee, the latter is not even an invitee. (ii) In January a panel set up by the Prime Ministers Office suggested replacing the requirement of approval by the relevant village councils (gram sabhas) with state government certificates that the Forest Rights Act (FRA) had been complied with. This would supercede all earlier Ministry of Environment and Forests (MoEF) circulars.[12] (iii) The Government issued a notification in December 2012 giving Coal India Ltd (CIL) the authority to directly approach the Central Pollution Control Authority, in order to boost the output of mines in operation since 1994 by as much as 25 per cent. This notification thus dispenses with the process of public hearings for these expansions.[13] (iv) In February 2013, the MoEF announced that clearance for linear projects (road, rail, power transmission, cables, and canals) would not require gram sabha consent in violation of the FRA. Further, 13 categories of infrastructure projects in 82 Maoist insurgency-affected districts have been exempted from requiring forest clearances. The same holds for public roads that require less than 5 hectares of forest land in those districts. (v) The MoEFs Forest Advisory Committee (FAC) has been clearing diversion of forest land at breakneck speed.[14] Among the proposals cleared: the JSW Steel mining project in the Saranda region of Jharkhand, from which security forces have been engaged in trying to evict Maoist forces.[15] (vi) The MoEF has agreed to de-link environmental clearances from forest clearances. Thus firms which have not yet obtained forest clearances for their projects can begin work on the non-forest segment. The Supreme Court has approved this de-linking. (vii) In the Vedanta case, regarding bauxite mining in the Niyamgiri hills of Odishas Kalahandi district, the MoEF has significantly changed its stance. Whereas it had earlier rejected the forest clearance for the project on the ground that it violated provisions of the Forest Rights Act and other Acts, on February 15, 2013 the MoEF said in court that the consent of the people would be required only in cases where displacement of large number of people is involved and which affect the quality of life of the people. The terms displacement of large number of people and quality of life were left undefined. Further, the MoEF affidavit said that for the projects for which diversion of such forest is unavoidable where rights of the forest dwellers are recognised, the rights may be circumscribed or extinguished using the eminent domain of the state. In this fashion it asserted that the Government and not the forest dwellers would have the final say in diversion of forest land for mining projects, regardless of the provisions of the Forest Rights Act.[16] Though the ministry continued to oppose permission for Vedanta to mine bauxite in the Niyamgiri hills, it has weakened its own case against Vedanta. The process of displacing and disenfranchising the forest dwellers has been facilitated by the large-scale rejection of tribals claims under the FRA. The official Saxena Committee report on the implementation of the FRA (December 2010) found that its implementation was very poor. As of December 31, 2012, 3.24 million claims have been filed under the FRA since it came into force in 2008; 1.28 million have been accepted, and a larger number, 1.51 million, have been rejected.[17] The process of filing of fresh claims appears to have ground to a halt. A recent study has found that the provisions for recognition of community forest rights under the FRA are largely unimplemented.[18] As the Minister for Tribal Affairs points out, Until youve settled rights, what basis will you compensate tribals on? Once you catch them by the neck and throw them out, theyre totally orphaned. The Minister of Environment has expressed her eagerness to cooperate in the PMOs drive to accelerate corporate plunder: We are a partner in the development of the country, and environment shouldnt be considered a roadblock. She points out that in the past one and a half years, 754 proposals out of 828 have been cleared by her ministry, involving the diversion of 18,200 hectares of forest land. Much more devastation awaits the forests: It is reported that proposals still pending involve the diversion of 57,469 hectares.[19] More important than the specific legal steps, however, is the overall climate of aggression and emphasis on results, regardless of the law, the effect on the environment, and the devastation of the lives of the forest dwellers. Forest land diversion has already taken place on a large scale (about 2 lakh hectares) since the FRA came into operation.[20] It is now taking place at an even more accelerated pace.

[2] Capital, vol. III, chapter 30. (back) [3] Citigroup chief stays bullish on buy-outs, Financial Times, 9/7/07, http://www.ft.com/cms/s/0/80e2987a-2e50-11dc-821c-0000779fd2ac.html#axzz2NaK4d7eb (back) [4] Budget to help India Inc save Rs 25,000 crore in two years, Business Standard, 2/3/13. (back) [5] See Aspects no. 45, pp. 20-24. (back) [6] David Harvey, http://socialistregister.com/index.php/srv/article/view/5811#.UVvBNfIZaHs (back) [7] Prabhat Patnaik, http://www.citucentre.org/monthly_journals/sub_topic_details.php?id=383&phpMyAdmin=3a7a0d985d532b349002380a96a45723 (back) [8] Amit Bhaduri, http://development-dialogues.blogspot.in/2008/02/amit-bhaduri-predatory-growth.html (back) [10]Nearly 1 lakh central forces to reclaim Maoist-held territory, Hindustan Times, 22/3/13 (back) [11] As pointed out by a public petition opposing the proposal for a National Investment Board (later converted into the Cabinet Committee for Investment), the Environment Impact Assessment Notification 2006, issued under the Environment Protection Act, 1986, requires that projects that potentially cause pollution, displacement, destruction of natural resources, etc., must go through a series of clearance steps informed by scientifically determined standards, public hearings and technical opinion of a variety of statutory agencies, both at the State and Central levels. The existing legal regime requires project developers to comply with various national legislations such as the Scheduled Tribes and Other Traditional Dwellers (Recognition of Forest Rights) Act, 2006, the Biological Diversity Act, 2002, the Environment Protection Act, 1986, the Air (Prevention and Control of Pollution) Act, 1981, the Forest (Conservation) Act, 1980, the Water (Prevention and Control of Pollution) Act, 1974, the Wildlife (Protection) Act, 1972, and a range of international treaties, as applicable. Failure to comply with the procedures or conditions relating to the environmental clearance regimes is a criminal offence punishable under the Environment Protection Act, 1986 and related environmental and criminal procedure laws. The Cabinet Committee seeks, among other things, to push aside these legal requirements. (back) [12] The Scheduled Tribes and Other Traditional Forest Dweller’s (Recognition of Forest Rights) Act, or FRA, was enacted in 2006 and came into force in 2008. This Act claims to undo years of injustice to these communities by recognising and vesting the rights to use, manage and conserve forest resources and to legally hold forest lands that they have been residing in and cultivating. In 2009, the Ministry of Environment and Forests issued a circular making FRA implementation and village council (gram sabha) consent compulsory before granting clearance for diversion of forest land. (back) [13] http://www.livemint.com/Politics/xFz088NmgMCUo4OXu6Xw6I/Environment-norms-may-be-eased-to-spur-investment.html?facet=print (back) [14] Forest panel on project clearance spree, Business Standard, 12/2/13. (back) [15] Sudeep Chakravarti, The Saranda business plan, Mint, 15/3/13. (back) [16] Source: http://www.downtoearth.org.in/content/centre-set-dilute-tribal-rights-over-forestland (back) [17] Status Report, December 31, 2012, Ministry of Tribal Affairs website (tribal.nic.in) (back) [18] Vasundhara and Kalpavriksh, in collaboration with Oxfam, A National Report on Community Forest Rights under Forest Rights Act: Status and Issues, http://www.fra.org.in/New/document/A%20National%20Report%20on%20Community%20Forest%20Rights%20under%20FRA%20-%20Status%20&%20Issues%20-%202012.pdf (back) [19] Forest panel on project clearance spree. (back) [20] A National Report on Community Forest Rights.(back)

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2015 by Research Unit for Political Economy |

|