No. 61, June 2015

| |

|

|

No. 61, June 2015 |

|

|

Nos. 61 Making Room in India – for Whom? Bank Board Bureau: Another Step toward Privatisation and Foreign Takeover Public sector banks: Reform by Death

|

Making Room in India for Whom? Major changes are under way in India’s defence sector. Prime Minister Modi claims that the defence sector is at the heart of his “Make in India” programme. He has announced his government’s intention to decrease the share of imports in arms purchases from 60 per cent at present to 30 per cent over the next five years. He claims the consequent increase in domestic production could create an additional 100,000 to 120,000 highly skilled jobs in India. Key to Modi’s plan is increasing foreign direct investment (FDI) and the involvement of the Indian private sector:

In his 2015-16 Budget speech, Arun Jaitley claims: “Our Government has already permitted FDI in defence so that the Indian-controlled entities also become manufacturers of defence equipments, not only for us, but for export.” There have always been two major components in India’s defence production: the foreign vendors and the domestic public sector units (PSUs). What “Make in India” does is to introduce a third component, that is, the domestic private corporate sector, which has hitherto accounted for only a trivial share. Will there indeed be, as Modi says, “room for everyone – public sector, private sector and foreign firms”? Whose share will decline to make room for the domestic private corporate sector? Raising the FDI cap It is unlikely that this step alone will bring in much FDI. Not only do foreign arms manufacturers maintain tight control on their technology for commercial reasons, but their governments place strict restrictions on any transfer of their technology, for strategic reasons. Armaments is by definition a strategic industry, that is, one in which the overall interests of the country’s ruling class prevail over the specific commercial interests of capitalists in that sector. Given the Indian rulers’ determination to outstrip Pakistan and rival China in armaments, they require the most sophisticated weapons they can obtain. If they cannot get foreign investors to make them in India, they have little option but to import them outright, or to witness only the last stage of assembly in India. This has been the long-established pattern. As for the Modi government’s dream of making India an export platform for foreign arms manufacturers (in the way China is for, say, consumer electronics), such globalisation of defence production has not yet taken place elsewhere. Nor is it likely that, in the near future, armed forces around the world will find “Made in India” stamped on the underside of their cannons or fighter planes. National defence industries are still the norm. There are some international production tie-ups, but these take place among treaty allies, essentially among NATO countries. (Incidentally, it is worth noting that the US, UK, and most EU countries maintain tight controls on foreign investment in their defence industries, keeping management in the hands of nationals or close allies.) It seems at any rate that the present increase of FDI cap is only a first step. The Government has always been aware that even those foreign arms firms that may consider investing here would insist on much tighter control in their hands. In 2010, under the UPA government, the Commerce Ministry had floated the idea of raising the cap to 74 per cent; when that was opposed by the Defence Ministry, the Commerce Ministry came back with the idea of raising it to 49 per cent, a step that was eventually taken by the present NDA government. In all likelihood, after some time, the Government will return with a proposal to raise the cap further. The August 2014 press note also mentions that, in cases where investments come bundled with state of the art technology, India will allow higher foreign ownership, up to 100 per cent; these will have to be cleared by the Cabinet Committee on Security on a case-by-case basis. Note that 100 per cent foreign ownership would seem to contradict the “room for everyone” mentioned by Modi. Indian corporate firms would not be happy being entirely left out. Apart from strategic considerations of their home countries, as well as their own desire to keep tight control on technology for commercial reasons, there is another commercial reason for foreign firms not to invest substantial sums in India. There is no assurance of a permanent market, as there is, say, for soap or automobiles, for which firms can roll out new brands/models every year or two. The Ministry of Defence would not be able to provide any purchase guarantee; and even if it did so informally, that could at most extend for the length of a particular order. How could it guarantee purchases of future weaponry from the same manufacturer? Meanwhile, foreign arms firms generally have idle capacity in their own countries, and there is pressure from home country politicians to maintain employment in those establishments. In these circumstances, all that seems likely is that foreign firms will import into India the major assemblies and perform some screwdriver operations here, without transferring any technology – much as they have always done with public sector firms in defence. Indeed, it is strange to hope that, by increasing the foreign share in joint ventures step by step, foreign control and imports would diminish. Under what compulsion are foreign vendors to cede control or cut imports? Defence procurement policy (1) ‘Buy (Indian)’— already available low-tech Indian products with a minimum 30 per cent indigenous content. (2) ‘Buy and make (Indian)’ – initial imports to be followed by local production by an Indian firm or by a joint venture with a foreign firm; eventual indigenous content in the whole contract must be at least 50 per cent. (3) ‘Make’ – where Indian public or private sector firms are capable of designing, developing and producing high technology complex systems or critical components/equipment for any weapon system through local research in a reasonable amount of time; minimum indigenous content of 30 per cent. (4) ‘Buy and make with transfer of technology’ – initial imports, followed by local production involving Indian firms capable of absorbing the technology. Finally, (5) ‘Buy (global)’ – outright imports, where there is no domestic capability or likelihood of its being developed. Any proposal to select a particular category must now state reasons for excluding the higher preferred category/categories.2 However, this official order of preference has not led so far to greater indigenisation, nor is it likely to do so. As can be seen from the above categorisation, even options defined as “Indian” may have fairly high import content (50-70 per cent). Making room for the Indian corporate sector

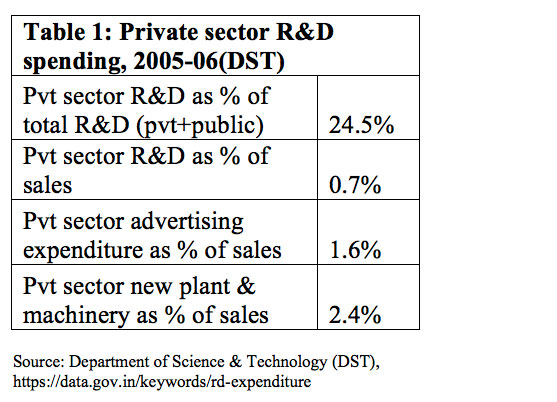

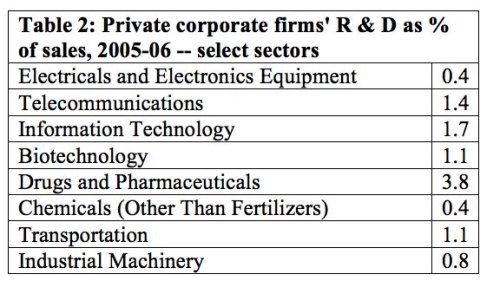

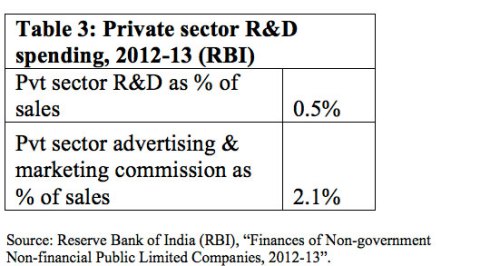

Technological capability of Indian corporate sector Indeed, the entire telecom revolution in India has been carried out with imported equipment, down to the handsets. The giant software sector in India has developed hardly any proprietary software, but merely operates imported software. Indian private corporate sector spending on R & D accounts for only a quarter of the country’s total R & D expenditure, according to Government data of the Department of Science and Technology (DST); the remaining expenditure is carried out by the much-maligned public sector. Moreover, according to two data sources (DST and the Reserve Bank of India), private sector firms’ expenditures on R & D are only 0.5-0.66 per cent of their sales. (See Tables 1 and 3 below.) Their expenditures on advertising and sales promotion are three to four times higher than their R & D expenditures. Nearly half (45.1 per cent) of total private corporate R & D expenditure in India is in just one sector, namely, drugs and pharmaceuticals; here R & D is a significant 3.84 per cent of sales. In India’s much-hyped Information Technology industry, however, R & D was only 1.7 per cent of sales in 2005-06 (the latest year available); in telecom, 1.4 per cent; in biotechnology, 1.1 per cent; electronics, 0.4 per cent; in chemicals, 0.4 per cent; and so on. (See Table 2)

So there is only one way of “making room” for the private sector, namely, by reducing the share of the public sector. Where the public sector has attractive assets – e.g., land in/near urban centres – these can even be transferred to the private sector for a song. Indeed, Jaitley mentioned in his Budget speech that his disinvestment revenues would include some “strategic disinvestment”; although he did not clarify what he meant, this was taken to mean outright sale of public sector units to private hands. In these recessionary times for the private corporate sector, when they have seen their profit rates flag, it is no surprise that they are enthused by the promise of both a steady market and the handing over of public sector assets to them.

NEXT: Bank Board Bureau: Another Step toward Privatisation and Foreign Takeover

Notes: 1. Modi at the Aero India show on February 18, 2015. http://indianexpress.com/article/india/india-others/live-defence-is-at-heart-of-make-in-india-programme-says-pm-modi-at-aero-india-inauguration/ (back) 2. Ministry of Defence, Defence Procurement Procedure – Capital Procurement, 2013, at mod.nic.in (back) 3. Anil Ambani, “Defence – where Make in India matters”, Hindu Business Line, 13/3/2015, http://www.thehindubusinessline.com/opinion/defence-where-make-in-india-matters/article6952076.ece (back)

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2015 by Research Unit for Political Economy |

|