No. 63, April 2016

| |

|

|

No. 63, April 2016 |

|

|

No. 63 (April 2016)

|

Private Investment: The God that Failed

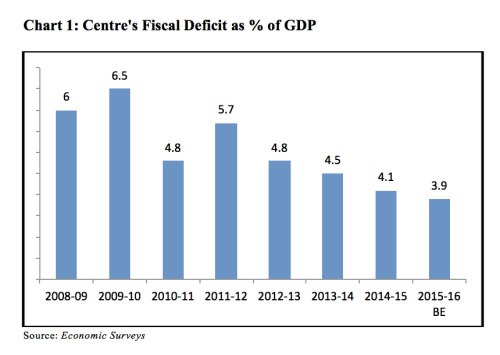

There is a new catch-phrase among the ruling circles: public spending. Over the last year, “captains of industry”, ministers, economists, bankers and financial journalists all appear to have become converts to the cause of increasing Government expenditure. In the last fortnight, their chorus has become almost shrill. What is even curiouser is that international credit ratings agencies Moody’s and Standard & Poor, staunch opponents of public spending, have not opposed this move outright.[1] This is a stunning about-turn from the days of the 2003-08 boom, when the same circles abhorred public spending, and depicted private investors as having virtually magical and limitless powers to conjure up funds and power growth. Even as recently as May 2014, they were convinced that Modi’s victory would revive corporate growth with a wave of ‘reforms’. The champagne of the 2014 victory is now flat. Now the captains are no longer confident that ‘reforms’ will revive corporate growth. It is worth looking into this about-turn for what it points to about a profound underlying problem of the political economy of India: namely, the problem of demand. The new votaries of public spending Pressure to raise Government spending has been coming from large industry. Sumit Mazumder, president of the largest business lobby, the Confederation of Indian Industry (CII), declared bluntly that manufacturing was at a two-year low, and the private sector would not invest, due to lack of demand. He asserted: “If required, we must go away from the stated path of fiscal deficit reduction in the interest of growth.” In other words, the Government needed to create demand for the private sector. The “path” of fiscal deficit reduction to which Mazumder referred is the one laid down by the Fiscal Responsibility and Budget Management Act (FRBM Act). Enacted in 2003, this Act dictates annual reductions in the fiscal deficit (i.e., total Government borrowing) till it gets to the level of just 3 per cent of GDP. This downward path has had to be modified repeatedly because of the slowdown in the economy following the global financial crisis of 2007-08. In his first Budget (2014-15), Jaitley promised to stick to the schedule set by his predecessor, of 3.6 per cent in 2015-16 and 3 per cent in 2016-17. In the 2015-16 Budget, however, Jaitley revised the schedule once more:

Despite slightly revising the timetable, Jaitley did indeed reduce the fiscal deficit in 2015-16; all he did was moderate the pace of reduction. As can be seen from Chart 1, the fiscal deficit has been steadily reduced for the past four years, first under the UPA, then the NDA. ‘Supply-side’ strategy What then was the growth strategy, devoid of stimulus from Government spending? At first, in May 2014, the corporate sector was confident that Modi’s huge majority in the lower house of Parliament would enable him to carry out sweeping ‘supply-side’ reforms, and thereby revive growth. That is, the Government would stimulate big capitalists’ desire to invest by increasing the profit rate in existing activities, protecting their profits against the downturn in economic activity, opening up new opportunities to make a profit, and handing over valuable assets for a song. For this purpose, at the top of the agenda were:

In respect of virtually all these the Modi government took urgent steps to fulfill its promises to its corporate backers. The Economic Survey 2014-15 (released in February 2015) proudly listed some of these anti-popular measures: the deregulation of diesel prices, increase in gas prices, taxation of energy products, labour ‘reforms’ (against the workers’ interests), the land acquisition ordinance, the near-freeze in crop procurement prices. Also listed were measures promoting privatization and foreign investment: a large disinvestment programme, the raising of FDI caps in defence, insurance, and other sectors, coal sector ‘liberalization’, and so on. In the case of passing legislation relating to land acquisition, the Modi regime has not yet fully had its way, even as actual acquisition of land has proceeded on the ground. Apart from the above, too, the Modi government has been straining every nerve to meet the demands of the corporate sector. It has exercised extraordinary pressure to effect sweeping changes in environmental regulations.[2] It set up a committee which recommended subordinating all environmental laws into a single Act, reducing no-go forest areas to a minuscule fraction, severely restricting public consultations and gram sabha permissions, and taking all submissions by project proponents on good faith.[3] It has sharply brought down the backlog of ‘stalled’ projects, and increased coal production by ignoring environmental objections.[4] It has made clear its intention to demolish most of the protections that exist, at least on paper, for industrial workers, and BJP-led state governments such as Rajasthan and Maharashtra have started the demolition at the state level. The Modi government has bent over backward to settle tax disputes in favour of foreign corporations. In the case of public-private partnerships (PPPs) which have turned unprofitable, it has permitted quicker exit for the private partners. Reigning dogma At some point, claim neoliberal economists, wages, input costs, and interest rates would fall low enough to make it profitable for capitalists to start hiring again and expanding production. And this cycle would proceed upward till full employment and full capacity. The market would clear, there would be no unused resources left, beyond the bare minimum necessary to allow flexibility. The natural state of the free market system, in their view, is full employment of resources; any temporary dislocation is quickly and spontaneously set right by market forces themselves. The only hitch, in the eyes of the adherents to this theory, is that there are political hurdles to the necessary price adjustments. Trade unions, or public employment programmes like NREGS, may prevent wages from falling to a ‘market-clearing’ price, and thereby prevent employers from hiring all the unemployed. Government procurement of certain crops prevents farmgate prices from falling. Public consumer subsidies on goods like foodgrains, fuel, or fertiliser make it unattractive for private capitalists to produce them, and thereby restrain growth. So too do explicit Government restrictions on foreign or domestic private investment in certain sectors. Once these hurdles are removed, say the supply-siders, the market will do the rest of the job of bringing about full employment. There is a reason why, irrespective of how poorly it performs in the real world, this dogma is kept alive. Namely, that it places the fate of the economy in the hands of the owners of private capital. Overall growth depends on theirinvestment decisions, and so the aim of economic policy is to excite their animal spirits by providing them ever more attractive money-making opportunities. In India, different state governments woo investors by providing them all sorts of concessions and subsidies. The Telangana government recently hit a new low, giving out full-page advertisements in the business press promising investors “Land on a platter” (accompanied by a picture of a plate loaded with biryani), and a novel right, the “Right to clearance” (!). Indeed all the other state governments too are engaged in this pathetic beauty contest, in which success is measured by the size of investments attracted, without looking at what has been done to attract them, or what effect the investments will have. If, on the other hand, the theory of spontaneous full employment is false, and State intervention in investment is regularly required even to keep things running as they are, that reality calls into question the social utility/relevance of the capitalist class itself: Of what use is the capitalist class if, even after being allowed by society to legally appropriate the social surplus, they cannot even deploy it to maintain ‘normal’ conditions of capitalism? Capitalists might answer: “How can we help it? Any individual capitalist who ventured to invest in such conditions would make a loss, since the demand does not exist”. But that merely underlines two facts: (i) in capitalist society there is an underlying demand constraint because of the poverty of the masses, the very masses who produce the social surplus; and (ii) socialised production is subjected to anarchy when investment is decided on the basis of private interest – sometimes resulting in an over-exuberant boom, sometimes in a depression. This means that, to rid the economy of crises, it is necessary to overcome the poverty of the masses and to establish comprehensive social control of investment. Such ideas are dangerous to the very ideology of private capital, for such social control can only be comprehensive by doing away with the capitalist. Thus, even though capitalist States have been forced at regular intervals to sideline the market-forces dogma in practice, they firmly adhere to it in theory, and return to practising it as soon as they get out of a slump. Corporate desperation In India, the facts are quite stark. After the onset of the global financial crisis in 2008, the Indian economy slumped. The Indian government then expanded the fiscal deficit sharply, and pumped huge credit to the corporate sector through public sector banks; growth revived, albeit with underlying weaknesses. Finally, from 2010-11, the Government went back to cutting the fiscal deficit, and the RBI raised interest rates. And then investment and growth slumped again. Ah, said the neoliberal economists, the mistake was in having tried earlier to revive growth through public spending. Instead, they say, the Government should have carried out supply-side reforms (of the variety mentioned earlier), which would arouse the animal spirits of investors. Indeed the Modi government upon coming into office strenuously tried to do this, but it became rapidly apparent that it was not working. In the fourth quarter of 2014-15, the private corporate sector’s sales fell 4.7 per cent, and its net profits fell by 12.5 per cent.[6]

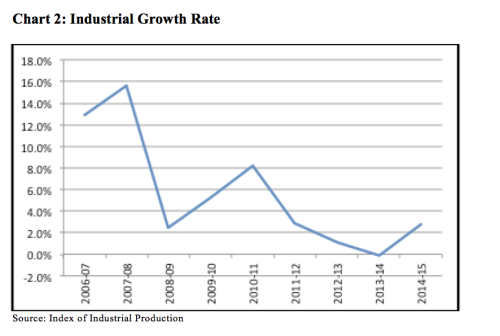

Since 2010-11 there have been four years of industrial stagnation. There was very modest growth (2.8 per cent) in 2014-15, but on a base of negative growth (-0.1 per cent) in 2013-14. Growth in April-November 2015 (over the corresponding period of the previous year) has risen slightly to 3.9 per cent, but this is still a far cry from the days of high growth.

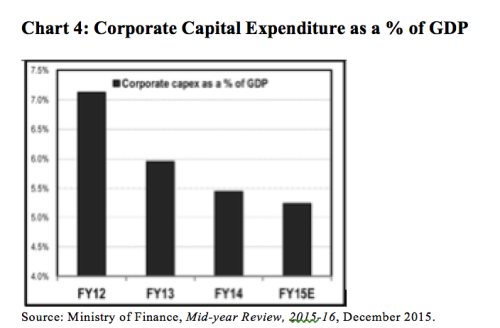

Taken as a percentage of GDP, corporate sector investment has in fact been in continuous decline, as seen in the following chart (Chart 4) from the finance ministry’s Mid-Year Review 2015-16.

The optimism generated among industrialists with the formation of the Modi government in May 2014 did not get translated into plans for capital expenditure. Not only did the RBI find a 27 per cent fall in envisaged capital expenditure by the private corporate sector for 2014-15, but the indications for 2015-16 are bleak.[7]Moreover, the Centre for Monitoring Indian Economy, in its surveys of capital expenditure by Government and the private sector, found that there was a sharp downturn in the quarter ending December 2015. Project commissioning in the December 2015 quarter, measured by value, dropped 44 per cent over the December 2014 quarter. Similarly, announcements of new investment intentions dropped by 74 per cent in the same period, despite having risen for the previous five quarters.[8]

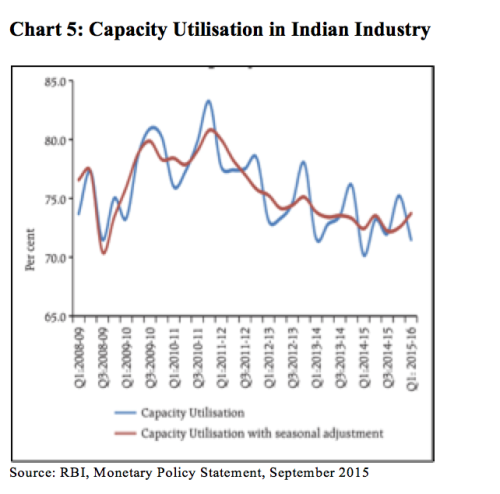

It is not surprising that private investors are not interested in setting up new projects, since there is large unutilised capacity in existing plants. RBI estimates put capacity utilisation in industry at below 75 per cent (the reading for April-June 2015 was 71.5 per cent; see Chart 5). In other words, vast productive investments are lying idle, a monumental waste all the more criminal in a capital-scarce and labour-rich country. Theoretical jugaad An orchestrated campaign began in December 2014, extending till the Budget. The three associations of large industry, CII, Assocham, and FICCI, met the finance minister to call for the expansion of public investments. A desperate Assocham went so far as to say, “Heavens would not fall if the fiscal target of 4.1 per cent in the current financial year is not met and the deficit moves up somewhat.”[9] But Indian big business was well aware that foreign investors and US-based credit ratings agencies, who call the shots, remain unrelentingly focussed on the reduction of the fiscal deficit. The new finance minister stuck to the 4.1 per cent target for 2014-15, set by the previous Government. Some other way out had to be found which would not technically breach the deficit target. Thus one demand from the ‘captains of industry’ was to make public sector firms spend their cash reserves (accumulated out of their past profits), and thereby boost demand. In December 2014, the three major associations of the private corporate sector pressed for the Government to compel top public sector firms spend their Rs 2 lakh crore (Rs 2 trillion) reserves, to “revive the investment cycle”. Note that, at the time when they were making this demand, top private sector firms themselves had Rs 4.6 lakh crore of cash reserves, which they were unwilling to invest, for fear that they may not make profits.[10] A second demand was for the Government to cut expenditure for the welfare and employment of the people, in order to make money available for public spending on ‘infrastructure’. This re-balancing of expenditure would boost corporate demand without raising the fiscal deficit. Indeed, the Government pursued this course actively. Subramanian’s solution Firstly, he frankly acknowledged that, contrary to the pre-election corporate propaganda, the large volume of private sector stalled projects was not on account of lack of regulatory clearances (what big business and the media called “policy paralysis”). Rather, it was because the earlier boom in investment had been a bubble, which had now burst. Subramanian cited data showing that the main reasons for the current stalling of major private sector projects was “Unfavourable market conditions” and “Lack of promoter interest”. He noted: “Perhaps contrary to popular belief, the evidence points towards over-exuberance and a credit bubble as primary reasons (rather than lack of regulatory clearances) for stalled projects in the private sector.” First attempt In February 2015, Subramanian had said that the only solution was increasedpublic investment:

One would hardly expect to hear such an argument from a neoliberal economist (i.e., one who believes that market forces, if “liberated” from State intervention, will efficiently allocate resources in the economy and ensure growth and full employment).[12] After all, one of the central tenets of neoliberal economics is that public investment ‘crowds out’ private investment, i.e., an increase in public investment hampers or reduces private investment. The entire policy of the Indian government for the last two and a half decades has rested precisely on this premise. Neoliberals argue that if the Government taxes and spends, taxpayers have less left to spend, thus reducing demand by the same extent; if the Government borrows and spends, its borrowing (i.e., increased demand for money) causes interest rates to rise, and thereby makes a number of private investments unattractive at the now higher interest rates.[13] Instead, neoliberals claim that the Government should simply remove all obstacles to private investment (e.g., laws protecting jobs, wage levels, the environment, small industry, etc.). The irrationality of this crowding-out theory, even within the frame of a capitalist economy, was long ago demonstrated by Keynes and others. When there is idle capacity and unemployed labour, and private investors are unwilling to invest for lack of demand, Government spending can revive demand and thereby crowds ininvestment. In fact, since Government spending results in a rise in the incomes of large numbers of people, who in turn spend part of that increased income, leading to a further rise in the incomes of other people, and so on, the eventual increase in demand is some multiple of the original rise in Government spending. The ratio of final increase in demand to the original rise in spending is called the ‘multiplier’. The multiplier also works in reverse: If the Government cuts expenditure, that results in a fall in the incomes of individuals, who in turn spend less, leading to a further reduction in incomes; the final decline in demand can be larger than the initial cut in Government spending. In fact, this is precisely the situation confronting India’s economy at present. Redistribution to the rich does not boost growth

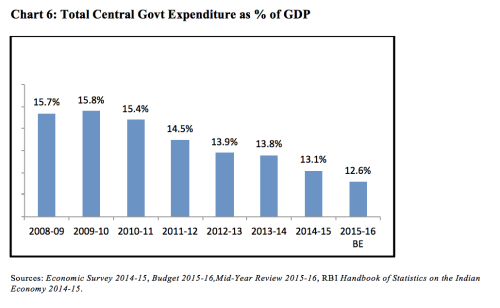

Rather, in the Economic Survey 2014-15, he said the solution was for the Government to slash certain types of spending, namely, spending on subsidies and welfare, and replace them with cash transfers to individual bank accounts.[15] This he termed “wiping every tear from every eye”. Cash transfers, he claimed, would put a stop to leakages, and exclude the better-off from the subsidies. The money saved by stopping leakages and targeting the poor better, he said, should be channeled into public investment in ‘infrastructure’. Thus, without increasing total Government expenditure, the Government could boost investment. The above argument is nonsense. Firstly, the conversion of various subsidies and welfare schemes into cash transfers will actually depress the real income of the working people. (We have discussed this in a separate article, “Constructing Theoretical Justifications to Suppress People’s Social Claims”.[16]) That will in turn depress demand for industrial goods. Secondly, since according to Subramanian’s initial proposal the increase in public investment would be at the cost of subsidies, the addition to aggregate demand would be nil. It would merely amount to spending less on heads which benefit the mass of people, and more on heads which directly generate demand for the corporate sector. Further, it should be remembered that the profits of corporations can be held in cash reserves, or be paid as dividend to rich investors, and the rich do not spend all or even most of their income. The common people, by contrast, spend more or less all of their income. Thus a transfer of this sort from the poor to the rich (and their corporations) actually subtracts from aggregate demand. And so Subramanian’s scheme cannot solve the problem plaguing industry at present, namely, the paucity of demand. It should be remembered that the present policy is not even to maintain the status quo, but to reduce expenditure further in line with the FRBM targets. The actual state of Central government expenditure is brought out in the following chart. Central government spending as a percentage of GDP has been declining continuously. That is, Government spending has been making a smaller and smaller contribution to demand.

Unsurprisingly, this starvation of demand has led to a prolongation and even worsening of the industrial slump. Second attempt

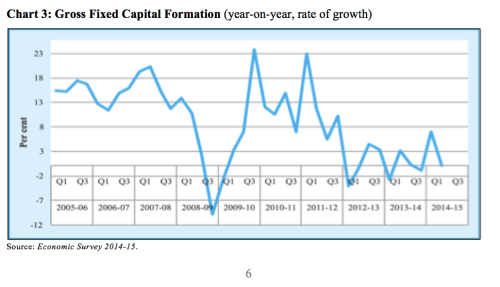

The MYR points out that “Recent international experience from Europe and elsewhere has shown that fiscal multipliers tend to be large especially at a time of contracting nominal GDP.” That is, since India’s nominal GDP growth is in fact declining, budget cuts would reduce GDP growth by a larger multiple than usual. The MYR conservatively estimates that a reduction of 0.4 per cent in the fiscal deficit will reduce aggregate demand by the same amount, and points out that there is little hope of any other source of demand, such as exports, stepping in to make up for this reduction. The above statements amount to a major confession: first, that the hallowed neoliberal theory of reviving growth by ‘supply-side measures’ (which amount, in essence, to providing more bounties to private capital) does not work; and second, that, in effect, the policies pursued by the Government in the current year are actually worsening the situation. The MYR brings out that industrial credit has slowed dramatically. Moreover, much of the industrial credit is going to sectors which are in distress: that is, rather than financing new projects, it is going toward dressing-up the accounts of deeply indebted firms. Growth in capital goods imports, an indicator of investment trends, has decelerated sharply from about 12 per cent in April 2015 to barely above zero by November 2015. Fixed capital formation, as a percentage of GDP, is three percentage points lower than the average rates recorded during 2011-12 to 2014-15 (and 10 percentage points below the peak reached in 2007-08). Demand is so depressed that the wholesale price index for manufactured goods is falling. In these circumstances, it is clearly irrational for an individual capitalist to invest; more money can be earned by simply keeping the funds in the bank than by producing goods and selling them at falling prices. It of course makes no sense for a capitalist to borrow, because interest rates are higher than growth in demand for industrial output. For the nation as a whole, too, declining nominal GDP growth (i.e., measured in terms of current rupees) means that the ratio of debt to GDP rises, and the burden of public debt becomes heavier in real terms. Thus, while the ratio of government debt to GDP had been declining for a decade, it is now in danger of rising. It is in these grave conditions that the MYR tacitly calls for an expansion of the fiscal deficit, or at least a halt to its path of reduction. As we mentioned earlier, the international credit rating agencies seem to have given a green signal to some such adjustment of the fiscal deficit reduction path, as long as it remains minor – say, half a percentage point of GDP. But such a small adjustment will also yield very small results, if any. By contrast, between 2007-08 and 2009-10 the fiscal deficit rose from 2.6 per cent of GDP to 6.5 per cent of GDP. That was the brief window of time in which, at the peak of the global financial crisis, international financial capital gave a green signal for fiscal deficit expansion everywhere. After all, that expansion enabled international financial capital to receive huge bail-outs, and return to solvency. Such a stimulus will not be easy for the Government to make today, since it would now face resistance from international financial capital and its local representatives; and they are positioned today to reverse any such measure. For example, if the Government were to expand the fiscal deficit in order to stimulate domestic demand, the Reserve Bank may decide to counter that stimulus by raising interest rates, suppressing demand. Moreover, foreign financial investors in India’s share and debt markets may start withdrawing their investments, negating any stimulus. As Raghuram Rajan puts it: “the international investor wants to be convinced that you will stay the course and you will disinflate because he or she prefers lower inflation rather than higher inflation. So we need at points of volatility to reassure them that this is indeed what we intend to do.”[17] That is, a policy of expansion of Government spending is incompatible with India’s actual dependence on foreign capital flows. Ending that dependence requires economic changes that call for a political will beyond the capability of the existing political-economic order. Of course, neither Subramanian nor his employers have any plans to disconnect from international flows of speculative capital, but Subramanian is aware of the harmful implications of this dependence. Indeed, just two years ago, before he joined the Government, he co-authored an article which sharply mocked the “foreign finance fetish” of developing countries:

But, in the various documents Subramanian has penned for the Government since 2014, there is a resounding silence regarding this dependence on foreign capital flows. Instead, these recent writings pat Indian policy makers on the back for successfully managing the external front. It is useful to track Subramanian’s successive revisions of his position: they show up the muddle created as the intellectual handymen of the ruling classes set their hands to the current crisis. But the demand problem is bigger than merely the immediate problem of reviving corporate profits, which is Subramanian’s main concern. It is necessary to consider why demand has collapsed in order to revive it reliably, and in a manner that is socially beneficial. Underlying problem of demand (i) The basic problem of demand in India is the narrowness of the market due to the endemic poverty of the masses. (ii) This narrowness in turn is related to the structure of employment, i.e., the fact that the overwhelming majority are trapped in low-productivity employment, while a small section are employed in so-called ‘high-productivity’ sectors. This is not a mere transitional phase, nor is it the result of overpopulation, or some adverse pattern of natural endowment, or some ‘vicious circle of poverty’. Rather the reasons for this dualism lie in the social structure: it is the result of parasitic extractions of surplus from the vast majority of labouring people, and the frittering away or unproductive drain of these surpluses. (iii) The most important cause of the dualism of employment is the longstanding failure to carry out profound agrarian reform, centered on the redistribution of land and other assets, cancellation of usurious debt, breaking of traditional monopolies of agricultural trade and credit (and their replacement with State assistance and popular control). At one time the need for land reform was universally acknowledged; now the very question is treated as outlandish, and not worth mentioning. In the absence of such agrarian reform, the vast peasantry, landed and landless, are left with little or no surplus; their surplus instead gets diverted to parasitic classes. Moreover, thoroughgoing agrarian reform is a pre-requisite for creating a free socio-cultural environment in which labouring sections can assert themselves and collectively develop agricultural and industrial production. This would include setting up local, labour-intensive small-scale industrial units suited to diverse specific conditions and markets. (iii) Thus as employment in India’s economy today is characterised by a baneful dualism, so is the market for goods and services. The corporate sector caters principally to the demand emanating from a relatively small section of Indian society (albeit large in absolute numbers), while capital-starved small units cater principally to the labouring masses, who lack purchasing power. (This division of spheres is not absolute: The corporate sector also encroaches on part of the market of the small units, and many small units eke out an existence in sweated subcontracting for the corporate sector.) (iv) By the late 1970s it was clear that the paucity of demand for mass consumption goods was restraining industrial growth. The response of the rulers has been to go in the opposite direction: to accelerate growth by delinking it from the needs of the masses and instead focussing (by and large) on the narrow elite market. This narrowness has three implications. Firstly, demand may expand euphorically for some time, such as the post-2003 period, when the middle and upper classes got easy credit to purchase consumer durables and flats. However, demand can thereafter get exhausted very suddenly, since it is not based on a real broadening of the market, but is a bubble. Secondly, given that the consumption basket of the upper-income sections contains a smaller share of labour-intensive mass consumption goods, and a larger share of items such as consumer durables and luxury services, less employment tends to get generated by industrial growth. Thirdly, given that elite consumer tastes mimic the tastes and brand loyalties of consumers in advanced countries, the share of foreign firms in industry rises, as does the import content. (v) The above features help explain the sudden surges and collapses of India’s industrial growth, its poor performance in job creation, and the persistent and growing negative trade balance of Indian industry. All three phenomena negatively affect demand for industrial goods and cause greater volatility. (vi) The liberalisation of imports since the 1990s has widened India’s merchandise trade deficit greatly, affecting demand in the commodity-producing sectors (agriculture and industry). On the other hand, in the 2000s there has been a shift in the composition of India’s exports to low value added primary commodities like iron ore, which create very little employment and merely enrich a few corporate barons. (vii) Another means the rulers have used to accelerate industrial growth is the promotion of private investment in infrastructure. However, this contains an inherent contradiction. Infrastructure involves large, lumpy investments with long gestation periods, and its costs get built into production costs in the rest of the economy. Private ownership of infrastructure, which tends to seek quick, high rates of profit, can be anarchic and damaging. (Railways in the 19th century are a classic example.) As a result, even economies wedded to free-market theories long deemed it prudent to keep infrastructure more or less in the public sector, at low, stable returns on investment. The present revival of private infrastructure in India, through ‘public-private partnerships’, has been at very high cost: through huge loans from public sector banks, large transfers of public assets and natural resources, outright subsidies, and so on. Even so, the PPPs as a whole have proved a disaster: some firms have shut down and defaulted on loans, many have stalled project work (as the demand scenario turned unattractive), others have deliberately underinvested and underproduced, and yet others have resorted to charging exorbitant tariffs. Excess capacity and debt built up during the infrastructure bubble now acts as a deadweight against any attempt at recovery. All these developments have actually wound up intensifying the demand problem and lowering industrial growth. (viii) The rulers are hoping that a fresh bubble will revive elite demand. However, they are aware that may take a long time; private accumulation cannot wait for that. In order to sustain the accumulation drive of large domestic and foreign capital even during a recession, the rulers are speeding up the transfer of land and other natural resources to the corporate sector; increasing hidden and explicit subsidies to corporate firms (by diverting funds from the social claims of the working people under PDS, NREGS, etc); and depressing workers’ wages and peasant procurement prices. (ix) These measures – the ‘Modi package’ – cannot be called stimulii as such; they are predatory. That is, instead of expanding the cake they attempt to re-carve the existing cake in favour of the well-fed. But their predatory actions have the effect of further depressing mass demand. And this has a further depressing effect on not only small industry and agriculture, but even, to an extent, on corporate demand.

Notes: [1] “India’s sovereign ratings not to be affected by deferring deficit targets: S & P, Moody’s”, Economic Times, 18/1/2016. [2] For example, see Nitin Sethi, “PMO ordered 60 changes to green clearances, environment ministry delivered on most”, Business Standard, 20/1/2015.http://www.business-standard.com/article/economy-policy/pmo-ordered-60-changes-to-green-clearances-environment-ministry-delivered-on-most-115012001495_1.html [3] See Ramaswamy R. Iyer, “A hasty, half-baked report on environment”, Hindu, 13/2/2015. [4] Nitin Sethi, “Only 35 of 793 coal blocks remain inviolate after dilution of policy”, Business Standard, 14/3/15. The dilution began under the UPA government; the NDA government brought the number down from 206 to 35. [5] When budget cuts were being imposed on southern European countries, the IMF hugely underestimated the depressing effect of such cuts. Its research department admitted its error, three years late. Olivier Blanchard and Daniel Leigh, “Growth Forecast Errors and Fiscal Multipliers”,https://www.imf.org/external/pubs/ft/wp/2013/wp1301.pdf [6] RBI, “Performance of the Private Corporate Sector during the Fourth Quarter of 2014-15 – Data Release”, July 1, 2015.https://rbi.org.in/scripts/BS_PressReleaseDisplay.aspx?prid=34326 [7] “Private Corporate Investment: Growth in 2014-15 and Prospects for 2015-16”, RBI Bulletin, September 2015. The capital expenditure already planned for the following year (2015-16) was 33 per cent lower than that planned for 2014-15 at the end of 2013-14. [8] CMIE, “Sharp drop in new investment announcements in Dec 2015 quarter”, 4/1/2015. CMIE, “Project commissioning declines in Dec 2015 quarter”, 4/1/2015. [9] “Heavens won’t fall if fiscal target is not met: Assocham”, Business Standard, 12/1/15. [10] “Push to get PSUs to invest surplus”, Business Standard, 23/12/14. [11] Economic Survey 2014-15, pp. 74-75. [12] Subramanian occasionally, and eclectically, toys with other approaches, but his overall frame of thinking remains resolutely neoliberal. [13] Another argument made by opponents of State intervention is that, as soon as the State increases expenditure, consumers fear that higher Government debt will result in a rise in taxes later; hence they save an equivalent amount, by curbing their expenditures. Therefore, they claim, increased State spending does not lead to the intended rise in aggregate demand. [14]Economic Survey 2014-15, vol. I, p. 50. [15] Of course, he couches this in appropriate language: “The debate is not about whether but how best to provide active government support to thepoor and vulnerable. Cash-based transfers based on the JAM number trinity—Jan Dhan,Aadhaar, Mobile— offer exciting possibilities to effectively target public resources to thosewho need it most.” [16] https://rupeindia.wordpress.com/2015/12/09/constructing-theoretical-justifications-to-suppress-peoples-social-claims/ [17] “Market fall not backed by fundamentals, says Dr Rajan”, CNBC, 20/1/2016. [18] Dani Rodrik, Arvind Subramanian, “Emerging markets’ victimhood narrative”,http://www.bloombergview.com/articles/2014-01-31/emerging-markets-victimhood-narrative

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

| All material © copyright 2017 by Research Unit for Political Economy |

|