No. 65, January 2017

|

|

|

No. 65, January 2017 |

|

|

No. 65 I. E-commerce: An Introduction II. Regulatory Issues & E-commence in India III. Employment Practices of E-commerce

|

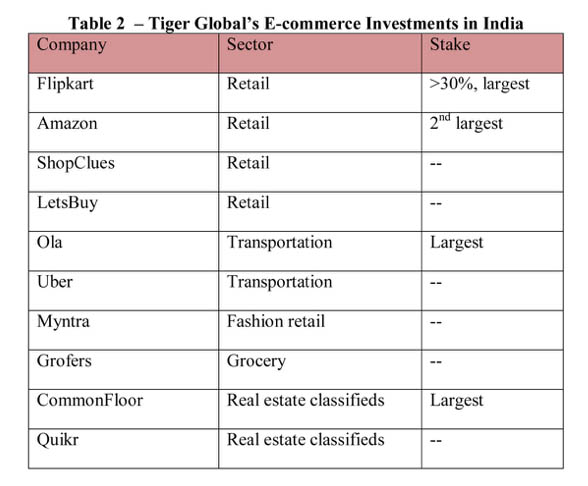

IV. The End Game: Towards Monopolisation and Financialisation If we summarise what we have discussed so far, it appears that apart from the hype and fantastic valuations as well as a few billionaires, e-commerce has little to offer– massive losses, degrading/unstable careers, and a regulation-evading industry. In this section we will probe deeper and attempt to make overall sense of the overarching strategy of the e-commerce industry and its investors. First and foremost, one medium to long-term plan that each of the dominant actors seem to be following is what is called ‘last man standing’ or ‘winner takes all’. The whole strategy is hinged on the idea that each of them will be able to finish or subdue the others to the point where only one or two of them remain as dominant players. So the whole idea is to burn cash and wipe out competitors before one really starts looking for profits. One can already see this process of consolidation taking place: while some new players are entering the fray, what has been happening for the last year or two is a strong movement towards mergers and acquisitions. Some of the prominent deals in recent years include: LetsBuy and Flipkart, Exclusively and Myntra, Flipkart and Myntra, Myntra’s recent acquisition of Jabong, OYO Rooms and ZO Rooms, Quikr and CommonFloor, Ola and TaxiForSure, Snapdeal and Freecharge, etc. Meanwhile, recently Ola has shut down its TaxiForSure (TFS) business and has laid off 700 employees in the process and Snapdeal decided to close Exclusively. Others who have gone under in the recent past include Tiny Owl, PepperTap, Zo Rooms, Purple Squirrel, Fashionara and Intelligent Interfaces.97 In grocery e-retail, while around 25 players have closed shop as of 2016, late this year, Amazon is reported to have elaborate plans to enter and capture the market.98 The number of mergers and acquisitions involving technology startups more than doubled from 69 in 2014-15 to 146 in 2015-16, according to data tracker Venture Intelligence.99 Experts are forecasting that start-up acquisition activity in 2016-17 will surpass last year's numbers, propelled by large funded companies such as Flipkart and Snapdeal on the one side and increasingly tight market conditions on the other. More revealing is the manner in which some of these deals have taken place. For instance, in one of the early consolidation moves Flipkart bought out electronics retailer Letsbuy.com for an estimated $25 million in 2012.100Since the time it started operations in 2009, Letsbuy deployed heavily discounted prices and extensive product catalogues as strategies to acquire market share. By early 2011, it had enough presence to convince reputed venture capital fund (VCs) like Helion Venture Partners, Accel Partners and Tiger Global to invest $6 million. But it burnt nearly all of it in less than a year. By the end of the year, it started knocking on investor doors for a fresh round of funds. However, by this time the investors had lost interest and were keen on salvaging their investments. Hence the founders were told by Tiger Global and Accel to sell their business to Flipkart. The Bansals of Flipkart, who have been substantially funded by Tiger Global (more of that below), were told to buy Letsbuy, and had no option but to acquiesce (though the official Flipkart line was that ‘Tiger had nothing to do with it’). At that time the company spokesperson assured that Letsbuy, along with its 350 member team, would continue to function independently and it could access Flipkart’s technology platform and supply chain capabilities. But in a few months, practically all of Letsbuy's 350 employees were quietly asked to leave and its infrastructure, including its warehouses, was dismantled. Accel and Tiger Global, however, could salvage all of the cash investments in Letsbuy and got additional stock in Flipkart. Thus we can sharply see here that the whole e-commerce story is very intimately connected with the strategies of the big investors and mechanisms of finance capital which practically remain invisible to the whole affair. It is to this question that we turn below. Underlying the e-commerce activity that we see around us in India are the so-called VCs (venture capitalists), whose activities are shrouded in mystery. Venture capital is the term used for funds provided at an early stage of a venture that has high promise and potential for growth. Despite this, a number of Indian e-commerce players like Flipkart, now almost a decade old and massive, continue being funded by ‘VCs’. Since all the key e-commerce players in India continue to be privately held, they are desperately dependent on VC investments in order to scale up their activities and even to continue their operations (given their massive burning of cash). Let us take the example of Tiger Global,101 perhaps the most ‘high-profile’ of such VCs in e-commerce in India. It is so publicity-shy that it does not even have a website. Founded in 2001 in New York, the company is part private equity fund and part hedge fund. It is one of the ‘hottest’ funds on the Wall Street, mainly because of its highly lucrative investments in Facebook (by which it is reported to have made $1 billion), as well as investments in other big Silicon Valley names such as LinkedIn. Tiger Global had raised more than $34 billion until December 2015, and made 171 investments in 109 companies, including 18 investments in India, often as a predominant player102 (see Table 2 below).

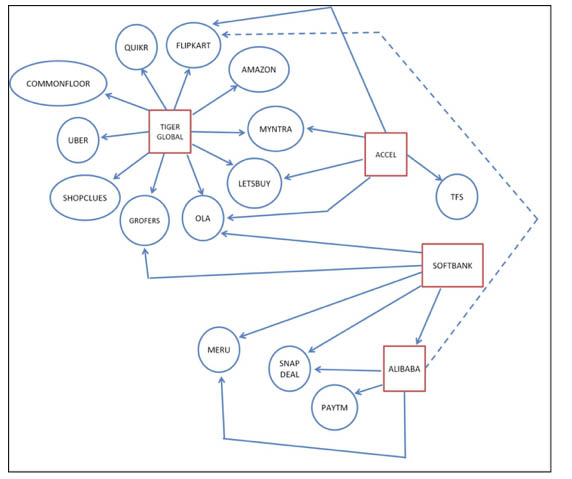

The table makes interesting reading. All this while we have been discussing how Flipkart and Amazon, Uber and Ola are in a fight to the finish against each other, but what we see here is that Tiger has significant, if not preeminent, interests on both sides of the battle.104 In fact, there are media reports that, on the lines of Letsbuy and Flipkart, there have been other competitors who have been pushed into consolidation, such as Flipkart and Myntra, Quikr and CommonFloor, so that Tiger could consolidate its holdings in all these companies.105 With an investment of more than $1 billion, Tiger Global has a stake of close to 30 per cent in Flipkart, and has been its biggest backer all these years. But even as Flipkart found itself in a tight spot since late last year, news emerged of Tiger Global's stake in Amazon, its second largest US stock holding, valued more than $2.1 billion.106 Of course the two investments have been done by two different arms of Tiger - the investment in Flipkart by the private equity business and that in Amazon by the public equity business. This makes one contemplate the ‘unthinkable’: a merger between Flipkart and Amazon, and complete domination of the newly carved e-retail market in India by such a combine, nudged by the interests of the likes of Tiger. This seems a possibility in the near future, especially if market conditions continue to tighten further. There has been serious speculation to this effect in recent months in the media, with potential and present investors drastically reducing the valuation of Flipkart from a high of more than $15 billion to nearly $9 billion, as it steadily loses market share to Amazon.107 On similar lines in April this year dna reported108 that Uber is close to acquiring a controlling stake in Ola, which will give it an almost 75 per cent market share (remember that Tiger now has stakes in both Uber and Ola). In June this year, Uber raised $3.5 billion funding from Saudi Arabia's sovereign wealth fund and promised to invest a ‘substantial portion’ on its India market. Uber’s India head claimed that the firm’s ‘war chest’ had more than $11 billion!109 In the most interesting – though not unexpected –development, Uber ‘sold’ off its China business to Didi Chuxing, the dominant ride-hailing service in that country, after losing some $2 billion in its China operations. The merger will create a $35 billion monopoly.110Last year Didi had created a global alliance with the US’s Lyft, India’s Ola and Southeast Asia’s Grab to create a global force to take on Uber; it had invested in Ola too. Interestingly, with this Uber - Didi merger, Uber becomes an indirect owner in Ola too, opening up possibilities for a China-like consolidation in the Indian market in near future. Pitted against Tiger Global is SoftBank, Japan's biggest telecom and internet company, with a huge investment arm including hundreds of startup investments across the world. SoftBank has been very active in India for the last couple of years, with investments of $2 billion. In the Startup India programme early this year its CEO announced that their investments in India will cross $10 billion in a few years.111SoftBank's investments in the past two years include $627 million in online-retailing marketplace Snapdeal (where it has the largest stake) and leading a $210 million funding round in Ola Cabs. It also paid $200 million for a 35 percent stake in InMobi, an Indian mobile-advertising network. Its other investments cover real estate website Housing.com, grocery retailer Grofers, and hotel aggregator Oyo. But SoftBank is also the largest shareholder in Alibaba, the home-grown e-retailer of China which is said to be the world’s largest retailer presently. Now Alibaba has bought significant stakes in Snapdeal as well as Paytm, India’s largest mobile wallet. Media reports suggest that even Flipkart approached Alibaba for its next round of funding.112Thus an alternate scenario is possible of SoftBank-Tiger rivalry being taken further through the Softbank-Alibaba umbrella - Snapdeal, Paytm and maybe Flipkart – coming together to fight Amazon in India. Figure 6 attempts to demonstrate the present picture of e-commerce investments in India and possible scenarios with Tiger and SoftBank in the centre of things (Accell is another influential VC). Dotted lines only show a possible line of investment. One aspect of the financialisation of these technology companies is remote control by VCs. Another aspect is the disappearance of their hefty revenues in a labyrinth of corporate structures remotely controlled from tax havens. As per a recent report113, Uber paid a paltry £22,134 in UK corporation tax in 2014-15 despite making a £866,000 profit, that is, a tax of 2.5 per cent.

In an expose recently, Fortune115 explains how Uber evades US corporate taxes. The strategy begins with Uber International C.V. (UICV; C.V. means partnership in Dutch), the subsidiary that Uber created in 2013. It has no employees and, though it is chartered in the Netherlands, lists the address of a law firm in Bermuda as its headquarters. It sits atop Uber’s network of subsidiaries outside the US. UICV agreed to pay the US parent Uber Technologies a one-time fee of $1 million plus a royalty of 1.45 per cent of future net revenue for the right to use Uber’s intellectual property outside the US. The two companies also agreed to share the costs and benefits of intellectual property (IP) developed in the future. This cost-sharing agreement effectively allows Uber to keep most of its non-US profits beyond the reach of American tax authorities. The second key Uber subsidiary in the Netherlands is a company called Uber BV (UBV).In fact, Uber has a total of 10 subsidiaries in the Netherlands, all of which share a mailing address in a nine-story building in Amsterdam. Seven of these companies, including UICV, have zero employees. But Uber BV, itself a subsidiary of another Uber offshoot, had 48 employees at last count. It has a lot of transactions to process: whenever a passenger takes an Uber ride anywhere in the world outside the U.S., whether it’s in Beirut or Bangalore, the payment is sent to UBV. The company typically sends 80 per cent of that ride payment back to the driver via yet another Dutch subsidiary and keeps the remaining 20 per cent as revenue. Here’s where things get interesting. UICV and UBV have an “intangible property license agreement” whereby UBV must pay a royalty fee to UICV for the use of Uber’s intellectual property –basically, the app that matches driver with rider. Under the terms of the agreement, UBV is to be left with effectively 1 per cent of the revenue after subtracting the costs of operation. The rest of the profits get sent to UICV as a royalty. And under Dutch law, that royalty payment is not taxable. The only sliver of UICV’s income that gets taxed is the royalty that the subsidiary pays to its US parent - the 1.45 per cent of net revenue it agreed to pay for the use of Uber’s IP in 2013. Thus, for every $10 in net revenue that UICV gets from UBV, it must pay 14.5¢ back to Uber Technologies in the US. That portion will be subject to US taxes. The rest of the income can just pile up in UICV’s coffers without being assessed. In addition to its Dutch companies, Uber has separate subsidiaries in each country where it operates. But those companies do not reap direct revenues from the rides taken locally. Rather, they function as “support services” businesses. Uber Italy, for example, gets paid by UBV to market the brand in Milan and Rome. Much of Uber Italy’s financing from Uber was made as a loan. The interest payments on that debt siphon off potential taxable income and are not taxed by Italy on the way out of the country because of a European Union directive. Similar is the case with Amazon, which is reported to be booking most of its revenues in the tax havens of Luxemburg and Ireland, evading billions of dollars in taxes in the US, Europe and elsewhere over the years.116According to a Mirror report last year, US tech companies, Facebook, Amazon, EBay, Apple and Google avoided taxes worth £1 billion by posting most of their revenues in tax havens.117 On a UK sale of £5 billion, Amazon paid less than £12 million in taxes in 2014. Apple paid a similar amount in tax for revenues of more than £10 billion in the UK in 2014. Thus all these piles of cash are then available to capture the global markets through the maze of corporate structures that are operated via tax havens.

Notes: 97. Nivedita Mookerji, “Why Ola, Snapdeal shut brands they chased and bought”, Business Standard, 18/08/2016, http://www.rediff.com/business/report/why-ola-snapdeal-shut-brands-they-chased-and-bought/20160818.htm, accessed on 10/10/2016. (back) 98. Karan Choudhury, “Amazon goes shopping for grocery partners”, Business Standard, 5/10/ 2016, http://www.business-standard.com/article/companies/amazon-goes-shopping-for-grocery-partners-116100400922_1.html, accessed on 10/10/2016. (back) 99. Biswarup Gooptu,“It’s the season of handshakes at startup Inc with Flipkart & Snapdeal seeking to make strategic purchase”, 26/5/2016, http://retail.economictimes.indiatimes.com/news/e-commerce/e-tailing/its-the-season-of-handshakes-at-startup-inc-with-flipkart-snapdeal-seeking-to-make-strategic-purchases/52443141, accessed on 23/06/2016. (back) 100. Rohin Dharmakumar, “Can Flipkart Deliver?” Forbes India, 6/7/2012, http://forbesindia.com/printcontent/33240 accessed on 24/06/2016. (back) 101. Diksha Madhok, “This secretive New York firm is quietly fuelling India’s e-commerce revolution”, Quartz India, 14/10/2015, http://qz.com/278550/this-secretive-new-york-firm-is-quietly-fuelling-indias-e-commerce-business/, accessed on 25/06/2016. (back) 102. “In Ola-Lyft-Didi-Grab alliance against Uber, curious role of Tiger Global is in focus”, Firstpost,14/12/2015, http://www.firstpost.com/business/in-ola-lyft-didi-grab-alliance-against-uber-curious-role-of-tiger-global-is-in-focus-2532814.html, accessed on 25/06/2016. (back) 103. Baid, op. cit. (back) 104. “In Ola-Lyft-Didi-Grab alliance...”op. cit. (back) 105. Shrutika Verma and Mihir Dalal, “Start-ups look for new backers as Tiger Global takes back seat,” Live Mint, 3/12/2015, http://www.livemint.com/Companies/6r5vDGPSyMom9z5NRZ5FhO/Startups-look-for-new-backers-as-Tiger-Global-takes-back-se.html, accessed on 25/06/2016. (back) 106. Digbijay Mishra & Shilpa Phadnis, “Flipkart's biggest investor also backs rival Amazon”, Times of India,18/11/2015, http://timesofindia.indiatimes.com/tech/tech-news/Flipkarts-biggest-investor-also-backs-rival-Amazon/articleshow/49823794.cms, accessed on 25/06/2016. (back) 107. Madhav Chanchani & Aditi Shrivastava, “Twist in startup tale: Flipkart and Amazon may have explored sale talks, say sources”, Economic Times, 16/3/2016,http://articles.economictimes.indiatimes.com/2016-03-16/news/71573460_1_binny-bansal-flipkart-and-amazon-sachin-bansal accessed on 25/06/2016. (back) 108. Praveena Sharma, “Uber may drive Ola away with controlling stake”, dna, 15/4/2016, http://www.dnaindia.com/money/report-uber-may-drive-ola-away-with-controlling-stake-2202187, accessed on 28/06/2016. (back) 109. “India to get substantial portion of Uber's $3.5 bn fund raise”, Times of India, 2/6/2016, http://timesofindia.indiatimes.com/business/india-business/India-to-get-substantial-portion-of-Ubers-3-5-bn-fund-raise/articleshow/52555872.cms accessed 11/08/ 2016. (back) 110. Athira A Nair, “Uber-Didi merger: Ola must be bothered, but guess who is excited about the development?” 5/8/2016, https://yourstory.com/2016/08/uber-didi-merger-ola/, accessed on 12/08/2016. (back) 111. “SoftBank's investments in India may surpass $10 billion”, Economic Times, 30/5/2016, http://economictimes.indiatimes.com/small-biz/startups/softbanks-investments-in-india-may-surpass-10-billion/articleshow/52499576.cms accessed on 26/06/2016. (back) 112. Shrutika Verma & Mihir Dalal, “Alibaba in talks to buy Flipkart stake”, Live Mint, 4/2/2016, http://www.livemint.com/Home-Page/qcQWDTZFoir7LpaGZZbnGP/Alibaba-looks-to-buy-stake-in-Flipkart.html, accessed on 26/06/2016. (back) 113. “Uber pays £22,000 tax on £866,000 UK profit”, Guardian, Oct 20 2015, https://www.theguardian.com/technology/2015/oct/20/uber-pays-low-uk-corporation-tax, the details of Uber’s tax evasion are primarily from this source accessed on 29/06/2016. (back) 114. Baid, op. cit. (back) 115. Brian O'Keefe & Marty Jones, “How Uber plays the tax shell game”, Fortune, Oct 22 2015, http://fortune.com/2015/10/22/uber-tax-shell/ accessed on 29/06/2016. (back) 116 .Tom Bergin, “Special Report: Amazon's billion-dollar tax shield” Reuters, December 2012, http://www.reuters.com/article/us-tax-amazon-idUSBRE8B50AR20121206, accessed on 29/06/2016. (back) 117. Nick Sommerlad, “Google, Facebook, Amazon, eBay and Apple avoided £1BILLION of UK tax”, Mirror, 26/1/2016, http://www.mirror.co.uk/news/uk-news/google-facebook-amazon-ebay-apple-7251746, accessed on 29/06/2016. (back)

NEXT: V. Making Overall Sense of the E-commerce Hype

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2017 by Research Unit for Political Economy |

|