No.s 66-67, May 2017

|

|

|

No.s 66-67, May 2017 |

|

|

No.s 66-67 (May 2017) I. Modi Govt’s ‘Pro-Farmer’ Claims II. Post-2004 Spell of Growth Over IV. Fairy Tales about Foreign Investment V. Insuring the Govt against the Peasantry VI. Ruinous Drive to Throw Agriculture to ‘the Market’ VIII. Tightening Grip of Parasitic Forces

|

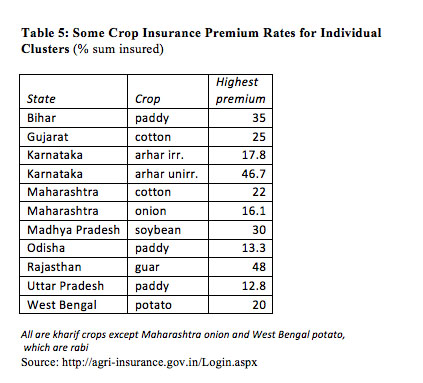

V. Insuring the Government against the Peasantry Before the Union Budget, the Government announced a new crop insurance scheme, the Pradhan Mantri Fasal Bima Yojana (PMFBY). This has been touted as a flagship programme of the Modi government in the agricultural sector, a ‘game-changer’, a solution to the problem of peasant suicides, part of a broader shift to ‘pro-farmer’ policies, and so on. The rationale for insuring peasants can hardly be questioned. Peasants face enormous insecurity in eking out a livelihood. Since they engage, even more than other sections of the workforce, with natural processes, they are particularly affected by the uncertainties inherent in such processes. In India, where 60 per cent of agriculture is rainfall-dependent, there have been five drought years since 2000. There have been other calamities as well, with losses running into tens of thousands of crores. In 2015 alone, the year began with unseasonal rains in 14 states, particularly in the northwest; July saw floods in parts of Rajasthan, Gujarat, and western Madhya Pradesh; in August, cyclone Komen struck West Bengal, and Bihar and Assam experienced floods; and the year ended with the south India floods (including most notably Chennai). Since peasants are very small operators in the market, they are at the receiving end of market fluctuations, and are unable to affect it by their actions. As shown both by the National Sample Survey data for 2012-13, the majority of peasants struggle to make ends meet, particularly in the absence of off-farm income. Without doubt, peasants need protection against all sorts of natural and manmade calamities. The question is, how. The real significance of the PMFBY lies not in the details of its benefits in comparison with earlier schemes, or how it could be improved further. While the government is trying to sell the story that the PMFBY seeks to address the “woes” of farmers, its purpose in fact is to absolve the State of the responsibility of securing the peasantry from calamity and distress. In line with neoliberal State policy, it touts a “market based solution” to the problem, one which will not solve the problem. Moreover, it takes a major step towards further privatising the insurance sector, handing a large and assured market to private players on a platter. Broad contours The scheme received a largely favourable reception from the corporate media (which are usually hostile to any subsidy or special provision for farmers, such as directed bank credit, subsidised fertilisers, subsidised electricity, etc). It is said to be an improvement on the existing crop insurance scheme in several respects. The premium to be paid by the cultivator has been reduced to 1.5 per cent of the sum insured on rabi crops, 2 per cent on kharif crops, and 5 per cent on commercial crops or horticulture. There is no upper limit on the subsidy to be given by the Government; even if the balance premium is 90 per cent, the Government will bear it. Earlier, the premium rate itself was capped, so that there would be a limit to the Government outgo on subsidy for the premium. As a result the sum insured was low, and correspondingly the claims paid to farmers were low. This capping has now been removed, so that the sum insured can be as large as the crop value itself. Now, it is claimed, the cultivator is to receive full cover, and the insurance company will collect the full actuarial rate (i.e., taking fully into account the statistical risk of claims). The sum insured will be determined by multiplying the average yield of the previous seven years with the minimum support price for the crop. The scheme will cover losses on account of natural calamities, including yield losses; losses due to prevented sowing; and post-harvest losses. It is claimed that it will use “technology” to speed up settlement of claims, presumably meaning photographs taken on mobile phones and the like. Whether or not it benefits peasants, the present scheme is certainly far more attractive to the insurance firms than earlier such schemes. (This explains why the corporate media have been so friendly toward the scheme.) The Government has notified 10 private firms for the PMFBY, along with some public sector firms (the Agricultural Insurance Corporation of India and the four public sector general insurance companies.)1 Only one insurance firm is to operate in each area/cluster, thus giving short shrift to the hallowed free-market principle of competition. In effect, it appears the firms will be provided captive markets at rates of profit guaranteed by State subsidy.Most importantly, the scheme covers only losses due to natural calamities; it does not cover the even more important man-made calamity of a fall in crop prices. Indeed, it is frequently the case that peasants suffer losses amid bumper crops. In the recent two successive years of drought (2014-15 and 2015-16) we witnessed an even stranger phenomenon in the case of many crops: a drop in prices despite a drop in production. This was due to the widespread depression of demand. Had the Government intended to protect peasant incomes at all, it would have provided comprehensive insurance against price volatilities and other market uncertainties. However, such a measure would have gone against the ‘free-market’ ideology and policies which are prescribed by global capital. (We place ‘free-market’ in quotation marks because an integral part of these policies is providing corporate firms and foreign investors guaranteed bounties, not subject to competition and other market uncertainties.) It is not clear how tenant cultivators and sharecroppers, who are in fact the poorest sections, can be beneficiaries of PMFBY: the overwhelming majority of tenancies are oral, with no tenancy rights, so the tenant would have no documents to submit. Of course, this lacuna exists even with existing Government relief measures for those affected by natural calamities. Broader significance of insurance What, indeed, is insurance? Among the dictionary definitions of “insure” are “to make sure or secure; to guarantee”, “to take measures to try to prevent an event leading to loss, damage, difficulties, etc.” and “to arrange for the payment of an amount of money in the event of the loss or theft of or damage to property or injury to or death of a person, etc by paying regular amounts of money to an insurance company.” The essence of insuring, then, is to secure a person/a group of persons against the risk of an adverse event; the ways one might do so are very varied. One can do so by preventing the event itself from taking place: for example, one can insure against floods by preventing deforestation, or insure against fires by fire-proofing a building. Another method of insurance is to minimise the damage that can be done by the event: for example, one can construct buildings capable of withstanding an earthquake; one can prevent construction on floodplains of a river; one can construct and maintain village tanks as an insurance against drought; and so on. Savings are also a form of insurance. Individuals routinely insure themselves against adverse events by saving out of their earnings. A rural collective may insure itself by setting grain aside for years of poor crops. A building society sets aside a sinking fund for various eventualities. The State is meant to take a variety of measures to protect the citizens against physical harm. (Indeed, the bourgeois theory of the State, as propounded by, say, Locke, is that it is a form of insurance created by a social contract: citizens delegate part of their rights to the State, so that it may defend them against injury.) But further, when the State guarantees certain goods and services to all citizens, that too limits the possible damage caused by an adverse event. For example, the provision of free universal health care insures a person against being unable to afford healthcare for lack of money. Public procurement of foodgrain is supposed to insure the peasant against a fall in prices to unremunerative levels; and public distribution is supposed to insure the citizen consumer against being too poor to obtain minimum nutrition. Indeed, public distribution is referred to by the likes of the World Bank as a ‘safety net’, which precisely is the meaning of insurance. The point is that the now common usage of the term “insurance”, to denote a financial contract between an individual and a profit-oriented firm, is merely one type of insurance, and not the better form. By the contract, the firm in a capitalist system promises to pay the individual a sum of money once a particular loss or injury has occurred. Such a sum, while better than nothing, is clearly inferior to preventing the event in the first place, if that were possible. It is also inferior to universal measures, which do not depend on whether individuals have had the money and foresight to purchase insurance, or on how quickly and scrupulously insurance firms settle claims. One should be clear, moreover, that the insurance policy is not the purpose for which the insured person pays a fee. The insured person cannot eat the policy document or use it to rebuild a collapsed building. The purpose is the settled claim, i.e., the actual payment obtained at the time of the injury or loss. So mere coverage of a particular number of people is not the criterion by which to judge the efficacy of insurance. Rather, we need to see whether it truly secures them against harm when they need it. Adversarial relationship There is no shortage of evidence of this adversarial relationship. Firms sell policies which are inappropriate for insured persons, in many cases resulting in the lapse of the policy, loss to the holder and gain to the firm. They avoid insuring persons whom they assess as high-risk. They sell policies which may prove useless at a time of real need. In theory, if the firm acquires a bad reputation, it will not attract customers, but customers even in developed countries lack information and the capacity to assess different firms and policies, and hence regularly fall prey to these practices; the “fine print” of insurance policies is a matter of lore, and the grist for John Grisham novels. In the developed world, insurance firms have also been reckless in their investment policies, thus endangering the insurance of their policy-holders. In the case of India, rampant mis-selling of life insurance policies by a host of firms during the period 2005-12 led to very large-scale lapse of policies, causing a loss to customers of Rs 1.5-1.6 lakh crore (Rs 1.5-1.6 trillion) and boosting the profits of the firms and the income of agents.2 This scandal led the insurance regulator to regulate certain insurance products, but the firms have suffered no serious penalties. (So appalling have been the practices and performance of private sector insurance firms since their entry in 2001 that they have reversed the pre-2001 trend of rising insurance penetration in India – i.e., insurance premiums as a percentage of GDP. Life insurance penetration has fallen sharply since 2006, and is now at the level of 2002, while general insurance penetration has stagnated at very low levels.3) While such a problem of mis-selling may not arise in the case of crop insurance at the moment, since at present there will be a single, standardised policy, this experience highlights the adversarial nature of the relationship and the sharp practices of firms. Losses borne by the public, profits channeled to the private sector Under the present scheme, private (and a few public sector) insurance firms bid for covering specific areas for a single season (six months) or two seasons (a year). They are not bound to cover them in the following season/year. Firms are meant to determine their bids on an actuarial basis, setting the premiums for each crop and area at a level deemed profitable in that season/year taking into account the probability of adverse events. The farmer bears a premium of 1.5 per cent of the sum insured for rabi crops, 2 per cent for kharif crops, and 5 per cent for commercial crops; the remainder of the premium is shared equally by the Central and state governments. Now, if the private insurance firm anticipates good rainfall, and therefore a low rate of crop failure, it may put in a bid to provide insurance at a reasonable premium, and thereby win the bid. Since fewer claims would be filed by farmers in a year of good monsoon, the private firm would be assured of a profit. In such a fashion, insurers reportedly collected a total premium of around Rs 16,130 crore under the PMFBY in the 2016 kharif season. It is also reported that total claims filed for the season amounted to only 60-70 per cent of premium collected.4In the case of Maharashtra, about Rs 4,000 crore was collected, of which only Rs 2,000 crore was paid out as claims.5 These are handsome profits for the insurance firms. On the other hand, if the insurance firm anticipates poor rainfall, it may not put in a bid at all, or deliberately enter a bid specifying such a high premium that it is certain not to win. Thus private insurers are backing out of the 2017 kharif season, since the monsoon is anticipated to be poor. In this year’s bidding in Maharashtra, which took place in March 2017, “most private players quoted exorbitantly high rates and outpriced themselves."6 As a result, bids for five clusters were won by public sector insurers, and only one was taken by a private insurer.In this fashion, profits are cornered by private firms, and losses by public sector firms. If the public sector firms too were to refuse to bid, the peasant would simply have no cover. In line with the adversarial relation we mentioned above, insurance firms are also complaining that the cut-off date for enrolling for the scheme is too late: by that date, the possibility of monsoon failure is known.7 Nevertheless, firms are lobbying for the Government to bear any claims in excess of 100 per cent of premium income – an even more explicit form of “losses to the public, profits to the private” logic inherent in the scheme. Although there is a wide range of winning bids in different regions and crops, even the winning bids can specify very high premiums. A few instances are given in the table below. Since the excess amount over the farmer’s share (which is between 1.5 and 5 per cent) is borne by the central and state governments, it is ultimately the public that is shelling out the remainder as a subsidy to the private sector.8

Why then does the Government need to hire an insurance firm to provide crop insurance? It might as well use its own machinery to assess losses and settle claims. Alternatively, it could direct public sector insurance firms to do the job, and subsidise their operations. Enthusiasts of private enterprise may believe that private insurance firms will do the job more quickly and efficiently than Government or public sector employees. Quite to the contrary, however, insurance firms have a strong incentive to keep down the amount paid out as claims; and as a matter of fact, among insurance firms, private sector firms have a much higher rate of rejection of claims than public sector firms.9 Presumably, this is due to the fact that a culture of public service, rather than a profit-maximising culture, lingers on to some extent in the public sector firms.It is not, therefore, on grounds of superior economic efficiency that the Government has devised the PMFBY. Comparing US and Indian crop insurance It is useful to compare India’s crop insurance scheme with that of the US. Despite covering most of US cropland today, crop insurance in the US still is highly subsidised by the US government. As with the new scheme in India, crop insurance in the US too (which covers not only yields but revenues as well) serves to channel subsidies and guaranteed rates of profit to insurance firms. Insurance covered only a small share of cropland in the US until, in 1994, subsidies were raised to very high levels. The US Department of Agriculture (USDA) pays 60 per cent of premiums, as well as overheads and a share of any catastrophic losses. The average total subsidy has been estimated at 80 per cent.10 As a result, crop insurance is highly profitable for the US insurance firms in this business; according to a study commissioned by the USDA, for the period 2000-08, the average rate of return on crop insurance in the US was 18.9 per cent, compared to an estimated ‘reasonable’ rate of return of 11.3 per cent.11 Before brandishing US crop insurance as the model for India, however, it is important to realise there is a world of difference between US and Indian farmers. The US has 125 million hectares of harvested cropland, but just 2.1 million farms. The large majority are not commercial farms: For 1.5 million farm households, less than 25 percent of household income comes from their farm. Large farms (of over 200 hectares) make up 11 per cent of the total, but account for 71 per cent of the cropland; 2 per cent of the farms account for 34 per cent of the cropland.12 It is the large farms in the US that are the main beneficiaries of the crop insurance subsidies as well as other subsidies, and the concentration of land with such giant industrial farms is increasing very rapidly.13 Indeed crop insurance is just one part of a web of subsidies to US agriculture. Price Loss Coverage provides price assurance to producers; Agriculture Risk Coverage protects farm revenues; Marketing Loan Assistance establishes minimum prices for most major farm commodities; and the largest scheme, the Supplemental Nutrition Assistance Program (earlier known as the Food Stamp program), has the direct and stated objective of disposing of surplus agricultural production. Total agricultural subsidies have risen from $74 billion in 2000 to $140 billion in 2012, and are set to rise further.14 That comes to over $65,000 per farm. In the US, median farm household income is considerably higher than the median income of all households, and this is much more so in the case of large commercial farms. For India, on the other hand, the National Sample Survey for 2012-13 estimates the number of ‘agricultural households’ at 90 million. It estimates that there are 109 million operational holdings, with an average area of 0.9 hectares each. Of these, 73 per cent are marginal (< 1 hectare), 15 per cent small (1-2 hectares), and 8 per cent semi-medium (2-4 hectares), accounting for 75 per cent of the land. There is a significant amount of tenancy, most of it oral. In tribal areas a large percentage of forest plots have still not been regularised. It is in this unorganised sector milieu, vastly different from that of the US, that crop insurance is meant to operate in India. Doubtless, Indian cultivators will be in a much weaker position to pursue their claims against the insurance firms than US cultivators. Moreover, crop insurance is one of the modes by which the US government actively funnels subsidies to not only the insurance industry but large-scale agriculture as well, using its economic and political clout to twist or defy WTO restrictions; and so there is little pressure to reduce the payments to its farmers, even if the costs are large. By contrast, the Indian government, lacking such clout as well as political will, is on the opposite course of reducing subsidies to agriculture, regardless of the consequences. Hence crop insurance in India will not be a means of funneling subsidies to agriculture. Indeed, the European Union, Canada, Australia and Thailand have signalled that they would consider India’s proposed crop insurance scheme a trade-distorting subsidy, to be counted within the overall WTO cap on such subsidies at 10 per cent of the value of agricultural production. (India could avoid this ‘trade-distorting’ label only by applying very restrictive conditions on the insurance: for indemnity to be payable, at least 30 per cent crop would have to be destroyed and a natural calamity would have to be declared.) It is possible the Government may solve this problem quite simply by reducing its various subsidies, including food subsidy, and replacing them with direct cash transfers – indeed, it has already taken this direction. Why PMFBY In line with neoliberal policy, successive governments of different parties have been withdrawing State intervention/assistance in different aspects of agriculture, and replacing them with ‘market-based solutions’. For example, by dismantling public sector agricultural extension services, the Government has left the field open for private sector extension services, i.e., private corporations or the local input trader. The gap in public sector bank credit to the rural population is to be filled by private sector micro-credit at exorbitant interest rates. Schemes and institutions for public procurement to prevent distress sales by peasants have been more or less wound up, and in their place the Government is promoting direct procurement by the corporate sector. Despite the callous conduct of the Government with regard to the peasantry, it has been unable entirely to shrug off such responsibility for delivering relief, both physical and monetary, in various conditions of distress. It therefore also faces the brunt of democratic peasant struggles, whether for procurement, compensation, or relief. For example, the UPA regime came to power in 2004 amid acute agrarian distress, and thanks to the votes of discontented peasants. It therefore was compelled to (partially) reverse earlier policies that had slashed public procurement of foodgrains, bank credit to agriculture, and public investment in agriculture. More recently, after the Prime Minister himself mocked the NREGS in Parliament and further slashed spending on the scheme during the drought of 2014-15, the Modi regime was forced to reverse its stand, and (partially, and very inadequately) restore NREGS spending. The Government continues to be held responsible by the organised peasantry for providing relief and assistance. To take a few examples from 2015-16: In October 2015 the Punjab government faced an extended agitation by peasant unions, including a prolonged rail blockade, to demand compensation for the devastation caused by the whitefly pest to the cotton crop; the state government had to face widespread condemnation as a result. In March 2016 tens of thousands of Karnataka peasants demonstrated in the state capital Bengaluru, jamming the main roads of the city. In Nashik (Maharashtra), tens of thousands of peasants blocked the main squares and roads in April 2016 demanding a loan waiver, better drought relief measures and compensation of Rs 50,000 per acre for destroyed crops. Such struggles are legitimate, in that the responsibility for protecting (‘insuring’) the peasantry ultimately lies with the State, whether it takes such measures preventively or in the form of compensation. With the PMFBY, the Government can claim that such woes of the peasantry have been addressed, and point them in the direction of the insurance companies. Crop insurance is thus a form of political insurance for neoliberal reforms, as well as a neoliberal subsidy to the private sector. This is precisely analogous to what the State is doing to public health: Arvind Panagariya, the vice-chairperson of the NITI Aayog, suggests that “for just three-quarters of a per cent of the GDP”, 0.76 per cent to be precise, “the government can provide at least a modest healthcare cover for the bottom half of the population” after which “there does not remain a case for additionally free provision of the service by the government”. As two experts in public health comment, “Such perceptions form the basis of an alternative for an eventual obliteration of the public services and in the process, lowering further the already low public spending in health."15 And just like private health insurers, private crop insurers will be laughing all the way to the bank. The insurance India’s agriculture needs Far from being an unproductive handout, such a comprehensive ‘insurance’ is a necessary guarantee of the country’s food security as well as the viability of the single largest source of livelihood. It is also of vital importance to expanding domestic demand for industrial goods. In brief, it is a necessary part of a national programme of development. None of this is on the cards, however. On the contrary, for almost all elements of such a comprehensive insurance, not only is actual provision today abysmal; the Government’s target is to eliminate what little there remains of them. And so the peasantry are to be buffeted not just by natural calamities, but by planned, manmade calamities. In those circumstances, the distribution of paper contracts to millions of small and marginal peasants is a cruel joke.

Notes: 1. New India Assurance, National Insurance, Oriental Insurance, and United India Insurance. (back) 2. Monika Halan, Renuka Sane, Susan Thomas, “The case of the missing billions: Estimating losses to customers due to mis-sold life insurance policies”, https://ifrogs.org/PDF/insurance-misselling_jepr.pdf (back) 3. Insurance Regulatory and Development Authority of India (IRDAI), Annual Report 2014-15. (back) 4. Rajalakshmi Nirmal, “Fasal Bima Yojana needs fine tuning”, Hindu Business Line, 6/4/2017. (back) 5. Namrata Acharya, “Extended cut-off dates hurt crop insurance scheme”, Business Standard, 8/4/2017. This is a bogus plea, since insurance firms made large profits in kharif 2016, despite the fact that a good monsoon was widely predicted, and materialised thereafter. (back) 6. Rajalakshmi Nirmal, op. cit. (back) 7. Namrata Acharya, op. cit. (back) 8. Some analysts claim that the premiums would come down once insurance firms cover, say, 50 per cent of cropland. It is true that insurance premiums tend to be higher when coverage is small, partly for the reason that those who opt for insurance initially tend to be those with higher risk (what is called ‘adverse selection’). Normally, risk is expected to decline as coverage becomes near-universal. However, in India this does not seem to be the case with existing crop insurance. Rather, existing coverage has been linked to public sector bank lending: cultivators are compelled to buy crop insurance when they take loans from banks. So it is unlikely that the risk of losses will decline as coverage increases. (back) 9. IRDAI, ibid. While the public sector LIC rejected only 1.2 per cent of death claims and kept 0.5 per cent pending, all private insurers had much higher rates of rejection and pending; Edelweiss Tokio was the highest, rejecting 37.8 per cent and keeping 5 per cent pending. There are similar gaps in the case of general insurance. (back) 10. Bruce A. Babcock, “Examining the Health of the US Crop Insurance Industry”, Iowa Ag Review, Fall 2009. (back) 11. Milliman, Inc., “Historical Rate of Return Analysis”, Risk Management Agency, USDA, 2009. http://www.rma.usda.gov/pubs/2009/millimanhistoricalrate.pdf (back) 12. James M. MacDonald, Penni Korb, and Robert A. Hoppe, Farm Size and the Organization of U.S. Crop Farming, USDA Economic Research Service, 2013. (back) 13. Ibid. (back) 14. Biswajit Dhar, Roshan Kishore, “Reality of US Farm Subsidies”, Economic & Political Weekly, 13/2/2016. (back) 15. Imrana Qadeer, Sourindra Mohan Ghosh, “Public health’s in the infirmary”, Hindu Business Line, 19/4/16. (back)

NEXT: VI. Ruinous Drive to Throw Agriculture to 'the Market'

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2017 by Research Unit for Political Economy |

|