No.s 66-67, May 2017

|

|

|

No.s 66-67, May 2017 |

|

|

No.s 66-67 (May 2017) I. Modi Govt’s ‘Pro-Farmer’ Claims II. Post-2004 Spell of Growth Over IV. Fairy Tales about Foreign Investment V. Insuring the Govt against the Peasantry VI. Ruinous Drive to Throw Agriculture to ‘the Market’ VIII. Tightening Grip of Parasitic Forces

|

IV. Fairy Tales About Foreign Investment During the past two years, the prices received by peasants for various agricultural products, such as potatoes, rubber, cotton, basmati rice, guar, eggs, and milk, have experienced sudden, even catastrophic, declines, in many cases to levels below the cost of production. In some cases, a steep rise in retail prices has been followed by a crash in mandi prices at the time when the peasant brings the crop to the market. The Finance Minister has not been much troubled by this phenomenon, and has limited himself to a few token interventions. In his 2016-17 Budget speech, however, he unveiled his solution to the problem: Our FDI policy has to address the requirements of farmers and food processing industry. A lot of fruits and vegetables grown by our farmers either do not fetch the right prices or fail to reach the markets. Food processing industry and trade should be more efficient. 100 per cent FDI will be allowed through FIPB route in marketing of food products produced and manufactured in India. This will benefit farmers, give impetus to food processing industry and create vast employment opportunities. As such, this is not a budgetary measure, since it involves no expenditure or taxation by the Government; it is a policy measure in place of the Government expenditure that should have taken place. That is, instead of the Government undertaking to protect peasants from post-harvest losses and exploitative traders and developing the necessary infrastructure to do so, the Finance Minister says the job will be done by foreign direct investment (FDI). The question assumes particular importance because horticultural production has increased considerably in recent years. Although some horticulturists are wealthy farmers with sizeable holdings and investments, the overwhelming bulk are poor peasants. In the effort to eke out a livelihood from small and marginal holdings, a growing number of peasants have turned to horticulture. (In the case of fruit, 90 per cent of the holdings, accounting for 50 per cent of the area, are of small and marginal farmers; in the case of vegetables, 87 per cent of the holdings and 58 per cent of the area.1) Over the last decade, area under horticulture has grown by about 2.7 per cent per year, and now covers 24.2 million hectares. During 2013-14, India’s production of horticulture crops was 283.5 million tonnes, which is higher than that of foodgrain crops.2 As an official committee of the erstwhile Planning Commission3 pointed out,

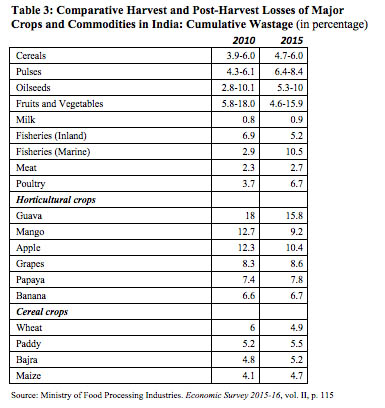

The report cites the case of the potato business, which is characterised by the crashing of prices during the peak season. The price disparity between peak and lean period arrivals ranges up to 100-150 per cent. Growers, particularly small and marginal farmers, are forced to dispose of output at a price which sometimes may not cover the cost of production. Unsurprisingly, this price pattern sometimes discourages farmers from cultivation. The market is in the grip of traders and agents who command large cold storage capacity spread over different states, and who are thus able to regulate the flow of supply to different markets. The picture for onions is similar. A study carried out for the Competition Commission of India in 2012 found that the onion market was characterised by cartelisation and hoarding. A few big well-networked traders, in collusion with intermediaries in other markets, control the markets. The study found that prices are unilaterally dictated by traders; farmers had a minimal role in price discovery (i.e., in determining prices through supply and demand) due to the low average size of their holdings – 1.15 to 1.3 acres.4 The tight grip of these cartels is experienced by consumers when the retail prices of onion soar periodically to Rs 40-80 per kg. For example, production in 2014-15 was 2.6 per cent below the previous year, but prices in September 2015 were almost double those of September 2014. What urban consumers may not realise is that, at other times, when the fresh crop arrives (three times a year), peasants receive Rs 8, 4 or even at times Rs 2 per kg. Although these prices are way below their costs of production, they accept them out of desperation. A few better-off cultivators have built storages and hold their crop till mandi prices rise, but the vast majority do not have such holding power or storage capacity. The Government’s response to the last onion crisis was to create a Price Stabilisation Fund of Rs 500 crore. This princely sum was meant to fund intervention to ensure remunerative prices for growers of not just onion but all horticultural crops. Just how derisory is the size of the fund can be seen from the fact that the NITI Aayog estimated the excess profits made by traders from the onion crisis of August-September 2015 at Rs 8,000 crore. The most that official agencies such as NAFED and Small Farmers’ Agribusiness Consortium (SFAC) spend on storing onions is Rs 100-200 crore. During the last onion crisis, NAFED and SFAC were provided interest free advances of Rs 8 crore and Rs 9 crore, respectively, to buy onions directly from farmers.5 Cartels in control During the spell of faster growth in the 2000s, cold storage capacity increased rapidly. Of the 28.7 million tonnes (m.t.) of cold storage capacity, nearly 14 m.t. were created between 2000 and 2011, to a large extent aided by Government subsidies (40-55 per cent of capital costs). However, this expansion of storage capacity does not necessarily help the cultivator. Nearly 96 per cent of the cold storages are in the private sector, largely controlled by traders/commission agents, whose model, says the report, is “based on price arbitrage; namely, buying cheap when arrivals peak and selling later when arrivals dry up.” Demonising APMCs: prelude to corporate sector entry Official criticism of APMCs serves merely as a prelude to advertising the virtues of corporate sector entry. To hear official reports tell it, corporates are charitable organisations dying to give cultivators a better deal, but are hampered by laws and regulations which prevent them from doing so. Exaggerated claims of post-harvest losses Had these claims been true, corporate investors, domestic and foreign, would long ago have seized the opportunity. Data in the Economic Survey 2015-16 reveal the figure of “35-40 per cent post-harvest losses” to be a wild exaggeration (Table 1 below). The highest rate of wastage is in the case of guava, 15.8 per cent; for most agricultural commodities wastage is 5-10 per cent.

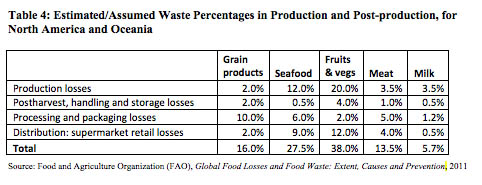

Even the figures given in the Economic Survey need to be questioned for the assumptions underlying the data collection. Produce that does not reach larger markets may not be wasted: it may be sold locally, or consumed, or put to some other use. In India, poverty ensures that very little gets actually wasted if the poor have some access to it. This, after all, is a society in which rag-picking is a form of employment. Since we are told that foreign investment in food marketing will reduce waste, it is instructive to compare India’s post-harvest losses with those of North America, as brought out by the UN’s Food and Agriculture Organization (FAO) (Table 2).

In the table for North America, we have excluded the largest component of waste in that region, namely, waste by consumers (this component is very low in the case of countries like India).6 It appears that, despite this exclusion, the US’s rates of loss are higher than India’s. The reason is precisely the corporatisation of food marketing, as a result of which produce that does not meet particular corporate standards is dumped before reaching the supermarket, and perfectly edible produce that has sat on the supermarket shelf a couple of days is dumped. Bringing foreign investment into India’s food marketing sector is hardly the solution to the problem of waste, to the extent waste is a real problem. Neither technology nor funds is the problem The cold storage gap as assessed by the National Spot Exchange in 2010 was 36.8 million tonnes, compared to an existing capacity of 24.3 m.t. at the time. This gap seems daunting, but keep in mind that between 1999-2000 and 2011-12, 15.4 m.t. of cold storage capacity was created with Rs 1,139 crore of financial assistance from the National Horticultural Board and National Horticulture Mission.7 The Planning Commission estimated the budgetary requirement for strengthening the farm produce supply chain at Rs 25,000 crore for the entire Twelfth Plan period (2012-17), or about Rs 5,000 crore a year.8 These are hardly large sums, considering that GDP from horticulture is now said to account about Rs 7 lakh crore (a third of agricultural GDP, or a little under 6 per cent of GDP). Nor is the task beyond Indian management skills; the success of a similar (and perhaps more complex) project, the building of milk cooperatives in Gujarat five decades ago, has proved that. What private investors want One can still find the odd, isolated instance of public sector intervention. Buried in an annex to the Planning Commission report is the case of a subsidiary of the public sector unit Container Corporation of India, Fresh and Healthy Enterprises Ltd (FHEL), set up to create cold chain infrastructure. Its main function at present is to procure apples from two districts of Himachal Pradesh, transport them to Haryana and distribute them to marketing firms and retail chains. The annex claims that

There is of course the much more conspicuous example of the Food Corporation of India, which, by guaranteeing procurement and distribution of rice and wheat, has for decades ensured a baseline income security to a sizeable section of peasants in certain states, a measure of insurance for the nation against drought, and grain for the Public Distribution System nationwide. (It is another matter that it has been weakened as part of systematic Government policy for the past 19 years.) It is precisely examples of successful public sector intervention that the Government wishes to eliminate at all costs, for it knows (and foreign investors bluntly state) that foreign investment will not come if there is scope for the Government to intervene in favour of cultivators or consumers. Such intervention might restrain private firms from making exorbitant profits, which is precisely what private investors are interested in. This insistence by foreign investors should itself provide us a clue of the likely effects of foreign entry in the food marketing sector. Will foreign investors enter to help peasants? Adam Smith claimed that “It is not from the benevolence of the butcher, the brewer or the baker that we expect our dinner, but from their regard to their own interest”. One might equally point out that it is not due to the wickedness of the trader that the peasant is impoverished, but due to their respective places in the system of social production, such that one can appropriate the labour of the other. The very helplessness of the small peasant before the trader, his/her lack of means and surplus, could as well be exploited by the corporate purchaser. At any rate, in the absence of very large farms, multinationals will go through the same intermediaries to procure crops. Once multinationals are established in the food marketing sector, they will pursue their global strategies, regardless of the effect on the Indian peasant or consumer. Even now, we have seen that the post-WTO opening of the Indian market has meant that global price trends affect Indian prices of goods; this would be all the more the case if global retailers have a strong presence here. Given the respective bargaining strengths of the peasant and the corporate purchaser, however, the effect may not be symmetrical: A drop in international prices could translate into a drop in the prices paid to the peasant here, without a rise in international prices translating into higher farmgate prices. On the other hand, global retailers could export commodities when global prices rise, raising prices for consumers. It is precisely the larger margins offered by complete freedom of trade that would attract foreign investors, and for that they want to be sure that the Government will not, and cannot, intervene in defence of Indian producers or consumers. Any attempt by the Government to intervene would likely be hobbled by the fact that it would by then have dismantled its own machinery for market intervention. Moreover, once the Government allows foreign retailers certain liberties, it would face pressure from foreign investors and foreign governments if it were to try to curb them. We have seen that attempts by the Government to collect legitimate taxes from multinational firms such as Vodafone, which set up elaborate structures to cheat the Indian exchequer, faced such pressure from foreign investors (and the British prime minister himself) that the Government more or less surrendered with its tail between its legs. Separating ‘agriculture’ and the peasant

The Aayog paper epitomises the ruling class approach, namely, that of separating the problem of agriculture from the question of the peasantry, and treating the latter as the obstacle to the former. The paper calls for (i) allowing the corporate sector to side-step the APMCs and procure directly from the cultivator (which will result in peasants in effect confronting a single buyer at the farmgate); (ii) replacing the policy of Minimum Support Prices (MSPs) with “Price Deficiency Payments”, whereby farmers would be given some support payments if the price of their crop fell below a certain threshold (this portends the dismantling of the entire system of public procurement); (iii) and a change in tenancy laws to provide a clear legal status to leasing of land. While acknowledging the criticism that a change in tenancy laws may “potentially hurt small and marginal farmers by restricting their access to land”, the NITI Aayog paper defends it on the ground that “more productive farms would create well-paid jobs that potentially provide better living than that of a small or marginal farmer”.10 No doubt well-paid jobs would be created for some people, but it is not clear what satisfaction the small or marginal farmer is to derive from that fact.

Notes: 1. Agricultural Census 2010-11, Table 6B. (back) 2. Economic Survey 2015-16, vol. II, p. 113. (back) 3. Planning Commission, Report of the Committee on Encouraging Investments in Supply Chains Including Provision for Cold Storages for More Efficient Distribution of Farm Produce, May 2012. (back) 4. “Competition panel finds price fixing in onions by cartels”, PTI, 7/2/2013. (back) 5. Sanjeeb Mukherjee, “Traders may have pocketed Rs 8,000 crore during onion crisis”, Business Standard, 7/10/2015. (back) 6. The FAO estimates food waste at the consumer level in industrialised countries (222 million tonnes) to be almost as high as the total net food production in sub-Saharan Africa (230 million tonnes). (back) 7. Planning Commission, op. cit., p. 85. (back) 8. Ibid., p. 76. (back) 9. Niti Aayog, “Raising Agricultural Productivity and Making Farming Remunerative for Farmers”, 2015. http://niti.gov.in/writereaddata/files/document_publication/RAP3.pdf (back) 10. NITI Aayog, “Raising Agricultural Productivity and Making Farming Remunerative for Farmers”, December 2015. (back)

NEXT: V. Insuring the Govt Against the Peasantry

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2017 by Research Unit for Political Economy |

|