No.s 66-67, May 2017

|

|

|

No.s 66-67, May 2017 |

|

|

No.s 66-67 (May 2017) I. Modi Govt’s ‘Pro-Farmer’ Claims II. Post-2004 Spell of Growth Over IV. Fairy Tales about Foreign Investment V. Insuring the Govt against the Peasantry VI. Ruinous Drive to Throw Agriculture to ‘the Market’ VIII. Tightening Grip of Parasitic Forces

|

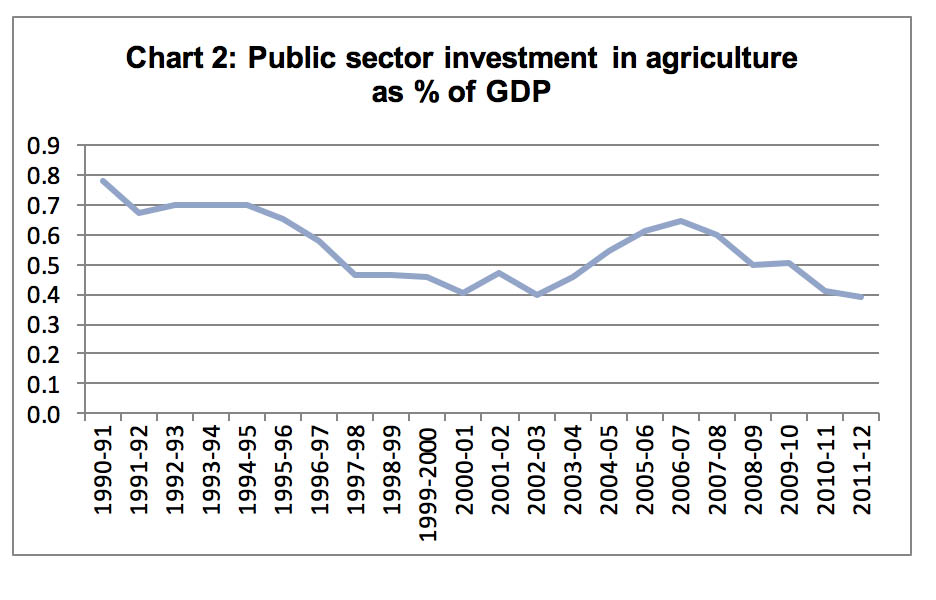

II. Post-2004 Spell of Growth Over Deeper crisis Agriculture accounts for nearly half India’s workforce (48.9 per cent in 2011-12). Yet its share of GDP is just 17.4 per cent (in 2014-15), and shrinking. The average income per person employed in agriculture (whether working on his own land, or rented land, or as wage labour) a little over one-sixth that for the other half of the workforce.1 So strong is the spell cast by ideology over establishment economists that they view the shrinking share of agriculture in GDP as signifying the corresponding decline in the importance of agriculture. Some even remark contentedly that droughts no longer depress India’s GDP as much as in the past. Presumably, then, if the share of agriculture in GDP were to sink to zero, we would be even further insulated from the effects of drought. These gentlemen fail to notice that GDP is merely an artifact, a measure of the incomes the existing social order assigns to different activities, regardless of their social utility or disutility; whereas food is a material thing, a human requirement for which a substitute has not yet been found. Given their outlook, it is natural that establishment economists and the corporate media imply that the only way to save the peasantry is to generate rapid growth in other sectors, and thus absorb the excess agricultural workforce into high-income jobs. In the name of this noble cause, then, governments at the Centre and the states woo foreign and domestic corporations, frequently by gifting them the land of the peasants they are being invited to save. Of course, this often involves using some force on the ungrateful peasants, garnering unsavoury publicity. How much better, then, to obtain the consent of the peasants by first rendering agriculture a losing proposition, so that they abandon it willingly. For those viewing things from this perspective, public investment in agriculture would be not only a waste of money, but positively an obstacle to progress, rather like repairing a building that you want to tear down. Spell of increased public spending and improved agricultural growth post 2004 Among these steps were the targeted doubling of rural credit in three years, rapid hikes in procurement prices, a rural employment scheme, expansion of rural roads, a partial revival of public sector agricultural extension and agricultural research, a National Horticulture Mission, and Government schemes aimed at improving productivity of rain-fed agriculture. Public sector investment in agriculture nearly doubled in real terms between 2003-04 and 2007-08.2 The UPA government also initiated the Bharat Nirman project to upgrade rural infrastructure (irrigation, electrification, roads, water supply, housing and telecom connectivity). Finally, it waived agricultural loans on a large scale in 2008-09. All these measures evidently had some positive impact, especially in the wake of the starvation of funds and credit under the preceding BJP-led NDA government.3 The UPA won a second term in 2009.

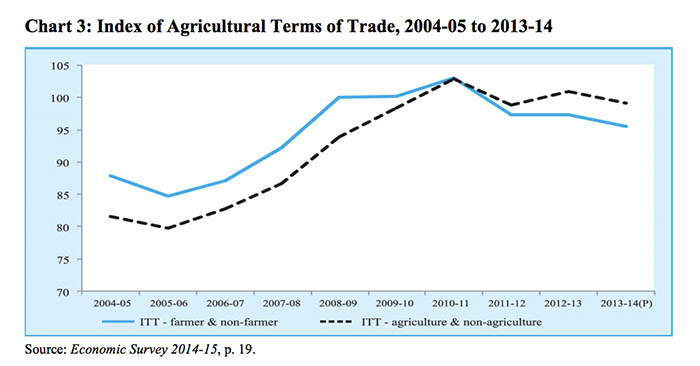

At least as important, however, in raising agricultural growth and returns post-2004 was the global economic boom of that period, resulting from the cheap credit policies of the US central bank. This flood of cash fueled demand and triggered rapid growth in many countries, including China and India. This in turn raised the prices of agricultural commodities worldwide, including in India. Accelerated growth also raised demand for casual labour in the construction industry. As a result of these two factors – Government policies relating to agriculture, and the economic boom – agricultural GDP growth rates rose, as did peasant incomes and rural wages. The terms of trade for farmers4 improved from 88 in 2004-05 to 103 in 2010-11. The official figures of farmer suicides showed a substantial decline.5

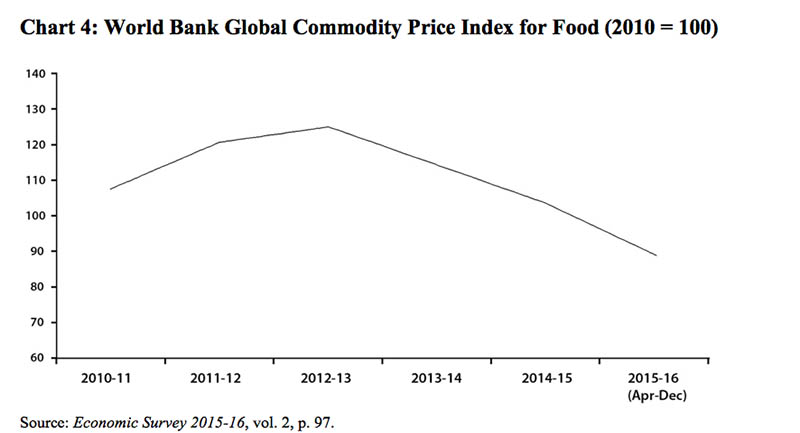

India’s economic bubble-boom did meet with a setback after the 2008 global crash; but the Indian government immediately responded to the needs of the corporate sector by expanding its own spending, providing tax concessions to business, lowering interest rates for a couple of years, and pressurizing the public sector banks to lend vast sums to private infrastructure firms. With an eye on the elections, it also waived agricultural debts and extended the MGNREGS to the whole country. All these steps helped revive aggregate demand and growth, and thus revived demand for agricultural commodities. Return to slump Moreover, after 2012-13, there was a downturn in the global prices of agricultural commodities (Chart 4); due to the globalisation of Indian agriculture, this had an immediate impact on Indian agricultural commodity prices. (It should be noted that, because traders are the dominant party in the peasant-trader relation, the effect of a change in prices is not symmetrical: while a rise in prices of agricultural goods does not get fully or quickly transferred to the peasant, any fall in these prices gets transferred immediately, and in full.)

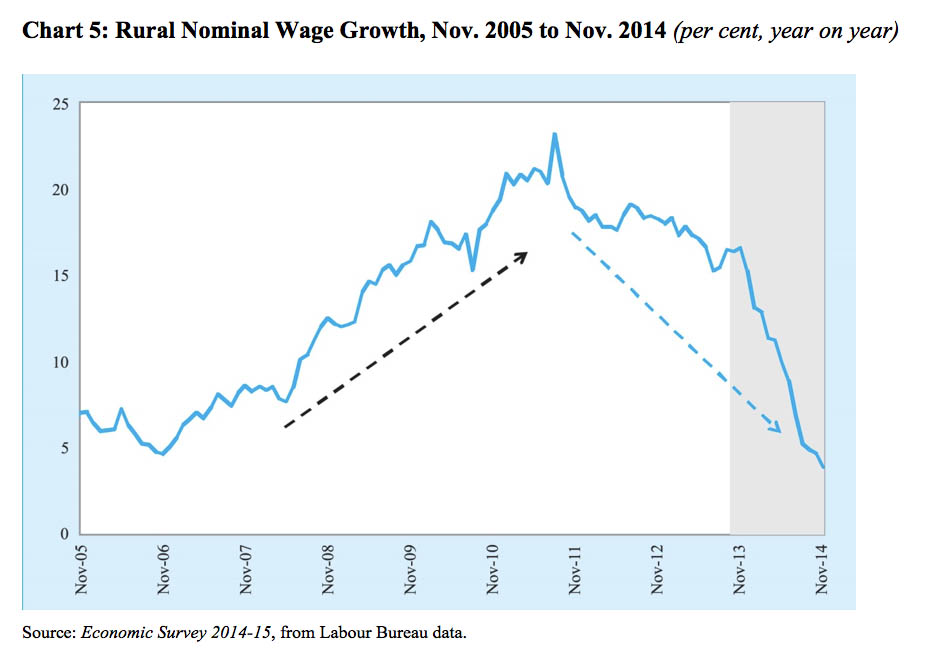

Investment (public + private) in agriculture and allied sectors, as a proportion of income in the sector, fell from 18.3 per cent in 2011-12 to 15.8 per cent in 2014-15. Terms of trade between farmers and non-farmers, and between agriculture and non-agriculture,6 began deteriorating from 2011-12. What this means is that peasants were once more caught between the price ‘scissors’ of rising input prices and stagnating/falling output prices. Subsistence agriculture (about 60 per cent of agricultural output is retained by peasants for their own consumption) would have come under even greater stress, since the rise in input prices would not even be partially compensated by a rise in output prices. Rural wages were depressed by a combination of factors, including a fall in farm employment, a slowdown in the construction industry, and the Government’s starving of MGNREGA. Rural wage growth started decelerating rapidly from the end of 2011, and turned negative in real terms (i.e., after discounting for inflation) by the end of 2014.

Depression of aggregate demand and peasant incomes In this context, talk of a ‘pro-farmer’ budget on the basis of a few increases in allocations for agriculture is meaningless. The overall situation of demand in the economy affects the peasantry, in the form of demand for, and therefore prices of, agricultural goods. As the national and global economy have sunk into recession, many prices of agricultural goods have stagnated or fallen in the past two years, squeezing peasant incomes. (Indeed, the phenomenon of peasant suicides has spread to more crops, such as potato.) Secondly, wage labour constitutes one-third of the income of a ‘farmer’ household,7 and a larger share in the case of those with small and marginal holdings. So the decline in real wages, due largely to the slump in construction, manufacturing, and agriculture, affects the peasantry.Therefore a Budget which constricts demand in an already recession-hit economy harms the peasantry, no matter if it is decorated with a few extra allocations for agriculture. The Chief Economic Adviser’s Mid-Year Review of the Economy (December 2015) pointed out that the Government policy of reducing the fiscal deficit in the present conditions was constricting demand and intensifying the recession. It frankly stated that fiscal deficit cuts “of the magnitude contemplated by the Government.... could weaken a softening economy.” Yet not only did the Government proceed thereafter to fulfill its commitment to fiscal deficit reduction for 2015-16, but it has adhered to the schedule of further reduction in 2016-17, in obeisance to foreign speculative investors and their credit rating agencies. This path of domestic demand-suppression no doubt reassures foreign speculative investors: such foreign speculators want to protect the value of their rupee holdings from the threat of inflation induced by a growth of demand. Moreover, they are eager to pick up assets at cut-rate prices in a depressed economy. However, this policy of demand-suppression has already depressed peasant incomes, and will do so further. The effects of this policy were apparent even before demonetisation. At the start of October 2016, it was reported that onion prices in the Nashik market had fallen to Rs 4/kg, and even lower.8 Moong dal was trading at 15 per cent below the official minimum support price (MSP)9 ; soya bean at 20-35 per cent below MSP10; groundnut at 35 per cent below MSP11; and raw cotton at 4-16 per cent below MSP.12 Thus the situation was already grave. Then, on November 8, the Government demonetised 86 per cent of the currency in circulation, striking an additional, and terrible, blow to demand even as peasants were marketing their kharif crops. Taking advantage of the cash scarcity, traders picked up potatoes, tomatoes, onions, peas, and other vegetables at below the cost of production.13 Pulses continued to be sold by peasants at well below the official minimum support prices, i.e., at unremunerative levels.14 Poultry farmers suffered a reported 40-50 per cent decline in sale prices in December.15 Two years of drought of rainfall were followed by a drought of demand. Even now, various Government policies combine to depress already feeble demand. For one, it appears that not all the cash withdrawn during demonetisation will be brought back into circulation (in an attempt to compel people to turn to cashless modes). Secondly, the Union Budget for 2017-18 prescribes further reduction in the fiscal deficit. Thirdly, the Reserve Bank is reluctant to lower interest rates, citing the danger of outflows of foreign capital. Thus the stagnation/recession experienced since at least 2011 seems likely to persist. This in turn depresses agricultural incomes. In the footsteps of the Raj It also extracted other such ‘invisibles’ payments such as profits on British investment in India. (iii) These payments swallowed up much of India’s trade surplus. (The financial mechanism by which this transfer took place was a bit more complicated, but we need not go into it here.) However, when agricultural prices crashed worldwide after 1929, India’s trade surplus vanished. The value of Indian exports plummeted from Rs 339 crore in 1928-29 to Rs 136 crore in 1932-33; meanwhile imports fell from Rs 263 crore to Rs 135 crore, leaving a merchandise surplus of only Rs 1 crore.17 How then was Britain to maintain the extraction of tribute from India? Another problem (or rather, another expression of the same problem) was: since crop prices had halved, how was land revenue to be extracted by the colonial administration, land rent by landlords, and interest payments by usurers, since none of these sums declined with the fall in crop prices? These burdens, always heavy, now became simply unbearable for the peasantry. (The concerns of Indian moneylenders and merchants, on the other hand, were reflected by G.D. Birla, who complained: “The moneylenders do not get back either the principal or the interest due to them.”18) The solution to both problems lay in going beyond surplus-extraction, by alienating the assets of the Indian peasant. Apart from their land, to which they clung as long as they could, the only assets the peasants had were gold and silver trinkets, their traditional form of savings. They were compelled to sell these to pay their revenues, rents and debts. Their meagre accumulations from generations of toil were now amassed and exported through the vast network of Indian moneylenders and merchants, at a tidy profit to the latter. Thus, while merchandise exports were no longer able to generate the trade surpluses needed to pay the Home Charges, exports of gold now did the job. Whereas India in 1928-29 made net imports of Rs 21 crore of gold, by 1932-33 it made net exports of gold of Rs 65 crore.19 The British gold reserve rose between 1932 and 1936 by 162 per cent.20 Even as incomes in India suffered a catastrophic fall, the colonial rulers maintained a brutal policy of income deflation and of strengthening of the currency.21 The colonial regime pursued the same expenditure-cutting policies as are enforced today; the difference is that today demand-suppression is justified by the slogan “fiscal prudence”; in those days it was “principles of sound finance”. Introducing the budget for 1931-32, the Finance Member of the Government of India, Sir George Schuster, said:

These words could almost have been taken from a speech of Raghuram Rajan. The colonial rulers’ demand-suppression policies internally boosted the value of the rupee; indeed the index number of wholesale prices in India fell more sharply than in Britain or the US.23 Moreover, while most other major economies followed a policy of devaluation of their currencies in order to protect their economies from import, India’s colonial rulers pegged the Indian rupee to the British currency at an artificially high rate.24 Internal deflation and a strong rupee reassured foreign investors that the colonial Government of India would be able to service its debts.25 However, this in effect multiplied the burden on the Indian people, in particular the peasantry. While a fall in the price level sounds as if it is a good thing, when prices are reduced by suppressing overall demand, it actually means a fall in the incomes of the working people, and a rise in the wealth of those who have financial assets. The fall in demand (i) creates unemployment, leading to a fall in workers’ wages, and (ii) leads to a fall in the prices received by peasants for their produce; both of these prop up the profit margins of capitalists, although it may not boost the absolute figure of their profits. On the other hand, the rise in the rupee’s value means that those with financial assets (denominated in rupees) can now command more real resources than in the past. That is, the programme is one of trying to bring about an economic recovery through giant transfers of income and assets from the working people to the owners of capital. This programme may not bring about a recovery, but it certainly brings about the transfer. Today, a similar policy of demand suppression is being followed by both the Government and the Reserve Bank of what is claimed to be a free India, under the instruction of foreign financial investors and their credit rating agencies. In the name of fiscal prudence and checking inflation, Government spending has been brought down steadily as a percentage of GDP, and the Reserve Bank has kept interest rates at elevated levels, even as the world economy and the Indian economy are in recession (whatever might be the claims of India’s official statistical machinery). In the last two years, input prices for agriculture have continued to rise even as crop prices have stagnated or fallen, for lack of demand. Where once the visible gauge of peasant distress was the outflow of gold, today it is the rising graph of peasant suicides. Meanwhile, the depression of demand has resulted in corporate sector sales growth falling since 2012-13, and since 2014-15 even the absolute figure of sales has been falling. Yet, thanks to the steep drop in the corporate sector’s input costs (a part of which consists of agricultural prices) and the slowdown in its wage costs, profit margins have risen during the last two years.26 Today, as in the past, the policy of cutting Government expenditure and keeping interest rates high is targeted at stabilising the rupee’s value. The aim is not to protect the real incomes of the masses, which are in fact depressed by the recession. Rather, it is to assure foreign investors that their financial investments in India are secure from inflation, even if that involves constricting productive activity here, and causing large-scale suffering. Raghuram Rajan, as RBI Governor, said candidly: “the international investor wants to be convinced that you will stay the course and you will disinflate because he or she prefers lower inflation rather than higher inflation. So we need at points of volatility to reassure them that this is indeed what we intend to do."27 In line with this, the Prime Minister recently went out of his way to announce to the visiting IMF chief, Ms. Lagarde, that India would not depreciate its currency as a method of boosting its share of trade vis-a-vis the rest of the world. He volunteered this assurance merely as a “good global citizen”, asking for nothing in return but the approval of the representative of international capital.28 Where the colonial rulers disgorged gold and silver from the peasantry, their present-day successors have handed over, and will continue to hand over, many precious assets of the country, frequently by disgorging peasants of their land. The peasant crisis of the Great Depression gave rise, within a few years, to the great waves of peasant struggles of the 1930s and 1940s. Perhaps the present conjuncture, too, will give rise to a fresh wave of peasant struggle, rather than merely more suicides; at least such is the need, and our hope.

Notes: 1. Economic Survey 2012-13, p. 32. (back) 2. At 2004-05 prices, public investment in agriculture rose from Rs 12,684 crore in 2003-04 to Rs 23,252 crore in 2007-08. (back) 3. B.K. Deokar, S.L.Shetty, “Growth in Indian Agriculture: Responding to Policy Initiatives Since 2004-05”, Economic and Political Weekly 28/6/2014.It should be noted, however, that much of the credit expansion that went under the name of agricultural lending was not to farmers at all. About one-fourth of the increase in agricultural credit during the 2000s was ‘indirect’ agricultural credit, such as loans to input/machinery dealers and corporate agribusiness firms. Even within direct credit, the share of loans to farmers fell from four-fifths in 2000 to less than half by 2011, the rest going to corporate agribusinesses and the like. Thus there was a rapid growth in the share of agricultural loans of over Rs 10 crore (!). By 2011 one-third of agricultural credit came from urban or metropolitan bank branches. After adjusting for this diversion of credit, the expansion of credit to farmers is unimpressive. – R. Ramakumar and Pallavi Chavan, “Bank Credit to Agriculture in India in the 2000s: Dissecting the Revival”, Review of Agrarian Studies, 2014. (back) 4. That is, the ratio of the index of prices received for farm products to the index of prices paid by farmers for inputs, consumption and investment. This measures whether farmers are, over time, getting more or less return in relation to what they spend. (back) 5. Ramesh Chand, Raka Saxena, Simmi Rana, “Estimates and Analysis of Farm Income in India, 1983-84 to 2011-12”, EPW, 30/5/2015. (back) 6. The first measure (‘farmers vs. non-farmers’), excludes agricultural labour from farmers (indeed it is purchased by farmers); the second measure (‘agriculture vs. non-agriculture’), includes agricultural labour in agriculture. (back) 7. National Sample Survey, Round 70, 2012-13. (back) 8. Amiti Sen, “No procurement relief for farmers”, Hindu, 1/10/16; Dilip Kumar Jha, “Onion price collapse makes farmers see red”, Business Standard, 3/10/2016. (back) 9. Dilip Kumar Jha, “Moong falls below MSP despite Govt buying”, Business Standard, 4/10/2016. (back) 10. Bhavika Jain, “After rains, soya farmers battle rock-bottom price”, Times of India, 27/10/2016. (back) 11. Rutam Vora, “As groundnut drops below MSP, farmers in Gujarat turn jittery”, Hindu Business Line, 27/10/2016. (back) 12. Vimukt Dave and Sanjeeb Mukherjee, “Centre starts procuring soya at MSP”, Business Standard, 27/10/2016. (back) 13. Editorial, “Problems of plenty”, Business Standard, 22/2/2017; Prabhu Mallikarjunan, “Too many vegetables, too little money: Prices crash post-notebandi”, Indiaspend, 18/1/2017; Vikas Vasudeva, “Cash crunch proves a hot potato for these farmers”, Hindu, 22/12/2016, and “Vegetables lose flavour in Punjab”, Hindu, 27/12/2016; Namrata Acharya, “Onion prices crash 40 per cent on bumper production”, Business Standard, 28/2/2016; Zeeshan Shaikh, “Nashik: Farmers getting Re 1/kg for tomatoes”, Indian Express, 12/12/2016. Also see Shreya Shah, “Flower Harvest Income Falls 70 per cent; Year Lost: A Farmer’s Story”, IndiaSpend, 17/12/2016, and Sohini Das, “Cash crunch slows down milk procurement in winter months”, Business Standard, 8/1/2017. (back) 14. Vishwanath Kulkarni, “As prices head south, tur dal farmers seek Centre’s support”, Hindu Business Line, 7/12/16; C.S.C. Sekhar, “Pulses sector heading for a crisis”, Business Standard. (back) 15. Dilip Kumar Jha, “Demonetisation: Poultry prices drop on weak consumer demand”, Business Standard, 6/12/16. (back) 16. The Home Charges consisted of the costs of British administration, the army, interest on Government debt and guaranteed payments to private British investors in railways. (back) 17. L. Narain, Price Movements in India (1929-57), 1957. (back) 18. Claude Markovits, Indian Business and Nationalist Politics 1931-39, 1985, p. 43. (back) 19. Narain, op. cit. (back) 20. R. Palme Dutt, India Today, 1947, p. 133. (back) 21. In metropolitan countries, governments tried to boost demand by increasing expenditure and devaluing their currencies; however, colonial India was not permitted either of these methods. (back) 22. A. K. Bagchi, Private Investment in India 1900-1939, 1972, p. 46. (back) 23. Markovits, op. cit., p. 42 (back) 24. The rupee’s exchange rate was fixed at 1 shilling 6 pence, whereas Indian manufacturers demanded that it be reduced to 1 shilling 4 pence. Indian manufacturers wanted a weaker rupee in order to protect them from imports. (back) 25. Bagchi, op. cit., pp. 65-66. (back) 26. The Reserve Bank notes that the private corporate sector experienced “Contracting sales growth but improved profit margins” in the first half of 2015-16. “Over a longer horizon, since the first half of 2012-13, aggregate sales growth recorded a declining trend.... Expenditure in the fi rst half of 2015-16 contracted due to contracting cost of raw materials and lower growth in staff costs. “Performance of Private Corporate Business Sector during First Half of 2015-16”, RBI Bulletin, February 2016. (back) 27. “Market fall not backed by fundamentals, says Dr Rajan”, CNBC, 20/1/2016. (back) 28. Our point here is not to argue for currency depreciation as a method of boosting the Indian economy. Rather, the point is that the present economic regime is geared to attracting foreign capital inflows. In order to do so, it becomes necessary for the rulers to keep the rupee strong, failing which foreign investors will pull out of rupee-denominated assets. In order to maintain a strong rupee, the rulers follow a policy of depressing domestic incomes. It is this assurance that the RBI and Modi are providing foreign capital. (back)

NEXT: III. Peasantry in Fetters

|

|

| Home| About Us | Current Issue | Back Issues | Contact Us | |

|

|

All material © copyright 2017 by Research Unit for Political Economy |

|